|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Edited by D. E. N. Dickson

International Labour Office

Geneva

This edition copyright © International Labour Organisation

1986

First published 1986

Fourth impression 1994

Publications of the International Labour Office enjoy copyright under Protocol 2 of the Universal Copyright Convention. Nevertheless, short excerpts from them may be reproduced without authorisation, on condition that the source is indicated. For rights of reproduction or translation, application should be made to the Publications Branch (Rights and Permissions), International Labour Office, CH-1211 Geneva 22, Switzerland. The International Labour Office welcomes such applications.

This publication was developed by the Improve Your Business project of the Management Development Branch of the International Labour Office, with financial assistance from the Swedish International Development Authority (SIDA), from an original idea conceived by the Swedish Employers' Confederation and published in Se Om Ditt F�retag (Stockholm, 1974). A preliminary test edition was published by the ILO in 1981.

|

Dickson, D. E. N. ILO Cataloguing in Publication Data |

The designations employed in ILO publications, which are in conformity with United Nations practice, and the presentation of material therein do not imply the expression of any opinion whatsoever on the part of the International Labour Office concerning the legal status of any country, area or territory or of its authorities, or concerning the delimitation of its frontiers.

The responsibility for opinions expressed in signed articles, studies and other contributions rests solely with their authors, and publication does not constitute an endorsement by the International Labour Office of the opinions expressed in them.

Reference to names of firms and commercial products and processes does not imply their endorsement by the International Labour Office, and any failure to mention a particular firm, commercial product or process is not a sign of disapproval.

ILO publications can be obtained through major booksellers or ILO local offices in many countries, or direct from ILO Publications, International Labour Off ice, CH-1211 Geneva 22, Switzerland. A catalogue or list of new publications will be sent free of charge from the above address.

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

FOREWORD

In recent years there has been an upsurge of interest in the role of small-scale enterprises as providers of employment and contributors to gross national product, and as a key component in economic development. This has been accompanied by the corresponding appearance of numerous publications on how to run small businesses. Given this, what is the justification for another book on the subject?

There are few publications which are simple enough to be understood easily by people with limited formal education but which can still communicate all the basic management knowledge required by entrepreneurs if they are to run small businesses successfully. This book is an attempt to fill this gap.

The underlying idea of the book is that improvements can best come from active and creative thinking by entrepreneurs about their own businesses. The purpose of this material is therefore to encourage such creative thinking and motivate entrepreneurs to take action to improve their businesses.

The material can be used equally well by individual business people or by trainers giving small business seminars and workshops.

The writing and publication of this book, as well as field testing of earlier versions in eastern Africa, was made possible by financial assistance from the Swedish International Development Authority (SIDA). The main author and editor of this edition of Improve your business is D. E. N. Dickson, ILO Chief Technical Adviser in Nairobi. He was assisted by Henny Romijn and Per Linden. Many of the ideas in the Handbook and Workbook owe their origin to the earlier work of the late Rhys Wynne-Roberts, who devoted so much time and effort to adapting the original idea conceived by the Swedish Employers' Confederation. Acknowledgement is also due to many other colleagues in the ILO Management Development Branch, the Kenya Industrial Estates and other organisations, for the comments and suggestions on how to focus and present this material.

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

WHAT IS IMPROVE YOUR BUSINESS?

Improve your business is about running small businesses. It has been written for retailers, wholesalers, manufacturers and operators of services such as repair services, laundries, dry cleaners and restaurants. Although in a small book like this we cannot hope to deal with the special conditions of each different trade, most of what we say can be used in many different trades or branches of industry. We have given examples from trade, manufacturing and service industries.

Improve your business is material for you to work with. It comes in two parts: a Handbook, which you are reading now, and a Workbook. They are best read together but they can each be useful if read separately. We recommend that you start using the Workbook and when needed turn to the Handbook for assistance.

Both the Handbook and the Workbook consist of eight sections, each of which deals with an important part of the management of your business. Each section of the Handbook has a corresponding section in the Workbook. The sections stand on their own and can be read separately.

A IMPROVE YOUR BUSINESS IS FOR:

RETAILERSWHOLESALERS

MANUFACTURERS

OPERATORS OF SERVICES

GIVES YOU MANAGEMENT IDEAS

THE HANDBOOK

The Handbook talks very simply about some of the important things that you must know and understand if you are to make your business work well over a long time. It is not a textbook, but you can get some interesting and useful ideas from the Handbook. The sections are set out in the same order as the sections in the Workbook, so that you can easily go from Workbook to Handbook or from Handbooks Workbook.

THE WORKBOOK

The Workbook will make you think hard about your business; it will do this by asking you a number of questions about your business and the way you are running it. In each section of the Workbook there is a list of simple questions to which you answer "yes" or "no". The answers you write will tell you how much you know about the strengths and weaknesses of your business.

The Workbook will also give you the possibility of learning more about the financial and practical sides of the business by means of simple exercises in business practice.

If you want to improve your management skills after going through the Workbook, you should then read the management ideas which we put in the Handbook.

TELLS YOU YOUR STRENGHTS AND

WEAKNESSES

WHERE TO START

We recommend that you start by going through the section which deals with that part of management which you think is weakest in your business.

If you do not know the strong and weak points in the management of your business, you can find this out by filling in the sheet called " Finding out your strengths and weaknesses" which is placed behind the introductory section, " For you in business ". We advise you to fill in this sheet before you start using Improve your business.

|

Note: Since this book is intended for use in many different countries, we have used the term " NU " in the examples to represent an imaginary " national unit of currency". |

|

| ||||||||||||||||||||||||||||||||||||||||||||||||

Improve Your Business: Handbook (ILO, 1986, 144 p.)

FOR YOU IN BUSINESS

It is for you in business that we have written Improve your business. Why? Because every business has scope for improving its sales and profits.

Figure

Even if your business is already doing very well, there are always things which can be done in a better way which you may not have thought of.

It is you, as the owner/manager, who has to make those improvements. You are the person who is responsible for everything that goes well and for everything that goes wrong in your business. You are also the one who sets the example to your employees.

All this means that you have to understand the working of your business very well, and also that you must be capable of putting that knowledge to good use by applying it in the actual management of your business. This is where Improve your business can help you. When you go through this Handbook you will acquire all the basic knowledge which you require to succeed in business. At the same time you will find that the material can help you to improve your management skills so that you can put your management ideas into practice.

Your aims in business

Before you start reading Improve your business, sit down for a while and think carefully about your business. Ask yourself what your aims are. Do you know exactly what you want to achieve with your business? Have you thought of what your activities in the market should be? Whom do you want to reach with your products or services? Do you know who your competitors are? Do you produce your goods or services in the most efficient way? Where do you want to go with your business in the future?

Having a clear idea about your goals in business is very important when you plan your business activities. Only if you know where you want to go will you make good use of your resources and be successful in business.

You and your business

To run any business means that you gather together things and people and put them to work to earn money for you. These things may be in the form of your own personal skill, the money you have saved, borrowed money, machines and raw materials and the skills of the people who work for you. If you are to earn your living from the business, then you must employ these things and people in a good way. This means that you must learn to think of these things and people as a separate group of assets called "the business". The business assets must be kept separate from your own private assets and from the members of your family.

BUSINESS AND

FAMILY: KEEP

THEM

SEPARATE

Figure

The business and profit

The major objective for being in business is to make a profit (or "a surplus", as some people prefer to say). Profit is made when the money which flows into your business is greater than the money which flows out. The greater the difference between money in and money out, the greater is the profit.

HOW PROFIT IS MADE

Now you know how profit is

made:

You and improve your business

If you read the ideas in this Handbook and think about them, you will know how to do two things:

1. You will know simple techniques which will help you to expand your market and increase your sales. Your sales will grow bigger, as you can see below:

Figure

2. You will understand what are the various types of costs which your firm will have to pay. By understanding these costs you will be able to keep them under control and maybe even cut some of them.

If you can learn to do this even in a small way, you will control the money which flows out of your business. Your costs will become smaller.

In these ways you will earn a greater surplus or profit from your business and you will make your business more successful.

Figure

Finding out your strengths and weaknesses

Before you start using Improve your business, you may wish to find out about your performance in business. You can get a rough idea about your strengths and weaknesses by answering the questions below. Each question concerns one area of management and corresponds to one particular section of Improve your business. For example, question 1 corresponds to section 1, question 2 to section 2 and so forth. Find out from your answers in which area(s) of management you are weakest and start reading the corresponding sections of Improve your business.

|

How good are you at... |

Good |

Average |

Bad |

|

1. Buying, selling and stock control? |

|

|

|

|

2. Production management and production technology? |

|

|

|

|

3. Bookkeeping? |

|

|

|

|

4. Costing and pricing your products or services? |

|

|

|

|

5. Marketing? |

|

|

|

|

6. Management accounting? |

|

|

|

|

7. Planning your business activities? |

|

|

|

|

8. Organising your office? |

|

|

|

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Improve Your Business: Handbook (ILO, 1986, 144 p.)

1. BUYING AND SELLING

All businesses must buy and sell to make a profit. The profit is made by buying at a low price and selling at a higher price.

· Good selling can increase your sales

· Good buying can decrease your costs

· This means: bigger profit

Retail and wholesale traders buy goods at a low price which they store, pack and distribute to sell at a higher price. This is the way they make a profit. They can work out whether they have made a profit (or a loss) in this way:

Figure

|

|

Sales of goods |

500 | |

|

Less: |

Buying costs of goods |

300 | |

| |

Difference or gross profit |

200 | |

|

Less: |

Other costs |

| |

|

|

Rent of shop |

60 | |

|

|

Wages |

100 |

160 |

| |

Surplus or net profit |

40 | |

Manufacturers buy materials and parts which they make into goods using labour, machines and power. They then sell the goods at prices which must be higher than their total costs. This is the way they make a profit.

Figure

Figure

Service operators sell services such as transport, repairing or cleaning. Like manufacturers, they use labour, machines and equipment and sometimes vehicles, fuel and power. The prices they charge for their services must be higher than their total costs. This is the way they make a profit.

Manufacturers and service operators can work out whether they have made a profit (or a loss) in this way:

|

|

Sales of goods or services |

|

500 |

|

Less: |

Buying costs |

|

|

|

|

Raw materials |

150 |

|

|

|

Labour |

100 |

250 |

|

|

Difference or gross profit |

|

250 |

|

Less: |

Other costs |

|

|

|

|

Rent for workshop |

60 |

|

|

|

Salaries and office costs |

75 |

135 |

|

|

Surplus or net profit |

|

115 |

Selling

The more you know about your customers and what they want, the more you will sell and the bigger can be your profit.

Retail and wholesale selling

The first step towards increasing your sales is to attract more people into your shop or store. Then, encourage them to stay and examine your goods, so that they buy as much as possible. To do this, your shop must be:

· well lit;

· clean and fresh looking;

· nicely decorated; and

· with the goods well displayed.

You should also have an attractive sign outside. None of these things take much money but they do help to increase your sales.

To sell their goods well, traders must:

· know who their customers are; and

· make sure they have the goods of the quality the customers want at prices they can afford to pay.

Figure

AN ATTRACTIVE

SHOP IS:

WELL LIT

CLEAN AND

FRESH-LOOKING

NICELY DECORATED

WITH THE GOODS

WELL

DISPLAYED

WITH AN

EYE-CATCHING

SIGN OUTSIDE

|

Note: People will buy from the shops which: · sell the goods of the quality they want at the lowest prices; · sell goods which other retailers do not sell. |

Customers must be able to see the goods they want. Sometimes retailers can make people buy the goods they want to sell by putting them at the front of their counters.

If your stocks of some goods are low, put them to the back of the shop. The people who really want them will ask. The others will not see them.

WHAT CUSTOMERS SEE, THEY WANT TO

BUY

Try to write down those goods which sell well and those which do not. In this way, you will understand better your customers' wants and you will not waste money buying goods which you cannot easily sell.

If there are other retailers selling the same goods as you in the town or in the market, go and see from time to time what they are selling. See whether-

· their prices are the same as or higher or lower than yours;

· their goods are better set out and easier to see;

· they have some articles which you do not have;

· the goods are of better quality than yours.

If you think some other shops do better than you, don't just copy them-do better still.

GET IDEAS FROM COMPETITORS

Industrial selling

Manufacturers or operators of services who know their markets well are more likely to be successful than those who do not know very much about their markets.

The most successful business people are those who study the market and set out to meet its demands.

What does your market look like?

You must find answers to the following questions:

· what the products are;

· who the customers are;

· where the customers are;

· how many customers you hope to sell to; and

· how much they buy.

Find out the answers to these questions by doing simple market research. Do the following:

talk to your customers;

ask what they like;

MARKET RESEARCH

MEANS:

LOOK, ASK, TALK

AND GET

INFORMATION

look at competitors;

look at what people buy;

get information about your products

or services.

Offer something different from your competitors, such as different sizes, different colours or different packaging. But do not be too different unless you are sure that it will sell.

Buying to sell

Before you can sell you must buy. How well you will sell depends on how well you have bought.

Intelligent buying can reduce your costs and make more profit for your business.

Retail and wholesale buying

Before you can buy you must know to whom you are selling and the sort of goods they want. As you have read in the section on selling: You must know your customers. Fora retailer or wholesaler, intelligent buying means to buy goods:

· of the types and sizes that your customers want;· at buying prices which are low enough for you to add a reasonable profit, while your customers are able to afford your selling prices;

· in quantities such that you have the goods in stock when needed, but not so many that your money is tied up for a long time.

GOOD BUYING MEANS

RIGHT TYPES AND SIZE

RIGHT PRICES

RIGHT QUANTITIES

If you are a small trader, you may have to buy in small quantities. Big traders who buy in big quantities can buy from manufacturers or get big discounts from wholesalers, but on small quantities you cannot get discounts. You may even have to buy from other retailers. Your profits will be small.

You may even be tied to one supplier who gives you credit. Even if you know that other suppliers' goods are better or cheaper, you cannot go to them because you are always in debt.

There is no easy way out of this. You already work very hard but this is not enough. You must use your brains.

Be hard on yourself and your family. Save every NU you can until you have enough to pay cash for your supplies and can choose your supplier.

Once you are free to choose your supplier, find out the ones who can give you what your customers will buy-and make sure you know what they want.

Compare what different suppliers can offer in the way of:

· prices;

· delivery;

· discounts;

· credit;

· quality; and

· something different.

Figure

DON’T BE TIED TO ONE SUPPLIER,

Figure

COMPARE SUPPLIERS!

Choose the supplier who gives you the best in terms of prices, quality and delivery.

Industrial buying

For manufacturers or operators of services, the way they do their buying has a big influence on whether their businesses are profitable. If they buy well, their prices can be lower, the quality will be better and they will be more competitive.

One way in which you can improve your buying is to break down your purchases into three groups as follows:

·

Raw materials (wood for the carpenter, cloth for the tailor)

·

Manufactured parts (locks, buttons for shirts)

·

Equipment for your own use (tools, etc.)

Raw materials need not be stored in your own storeroom. You can often make a special arrangement with your supplier so that you can have the raw materials delivered just when you need them. In this way, you do not tie up money for storage. If raw materials are in your store-room too long, sell them off even at cost price. Manufactured parts are often cheaper if they are bought in larger quantities. If you can buy one dozen, this will be cheaper than if you buy one single item.

Can you buy bigger quantities jointly with other people and get a discount for quantity?

Tools and other equipment for your own use must always be available. When they are broken, replace them immediately.

Figure

HOW TO BUY

|

1. Examine your needs |

|

· How much do I

need? |

|

2. Find the supplier |

|

· Look in telephone

book |

|

3. Ask for quotations from several suppliers |

|

· Telephone

them |

|

4. Negotiate terms and then buy |

|

· Talk with each

supplier |

|

5. On the day the goods arrive, check quantity, quality and price against delivery note |

|

· Check all

deliveries |

|

6. If you have any complaints, complain to the supplier immediately |

|

· Contact the supplier

himself |

|

7. Check your invoices against the delivery note when it arrives |

|

· Check the

prices |

Lastly, there are always new materials, parts and tools being introduced. Keep yourself up to date.

Stock control

Stock control means keeping a check on your stock of goods, materials and parts. With good stock control you can:

· make sure you do not run out of stock;

· make sure you do not hold too much stock of any item.

TOO LITTLE STOCK

Why your business can run out of stock:

· because you have forgotten to order goods or materials to replace those sold or used:

· because you have ordered too late;

· because you did not know stocks were low.

Why it is bad to run out of stock:

· because if you run out of stock and must say "no "to customers, they may go to competitors and may not come back to you again.

Why your business can hold too much stock:

· because you do not know which of your goods are not selling well, and stocks are piling up;

· because you do not know how much stock you have, if your stock is not easy to see and count;

· because you do not check regularly how much stock you have in your store.

Why it is bad to hold too much stock:

· because if you keep much larger quantities of stock than you need, you have tied up money which you could be using more profitably.

TOO MUCH

STOCK

The rules of stock control

RULE 1 - CHECK YOUR STOCKS REGULARLY

How often you do so-once a month, once a week or even once a day-depends on your type of business, how fast your stocks move and how much stock you keep. If you keep your stocks at low levels because you want to keep down the amount of money tied up, you must check often.

CHECK STOCKS REGULARLY

Take note of goods and materials which are selling fast and those which are selling slowly.

RULE 2 - SET OUT YOUR STOCKS WELL SO THAT THEY ARE EASY TO SEE AND COUNT

If the stocks are mixed up, they will not be easy to see and will be very difficult to count.

Stocks mixed up

Stocks well set out

SET OUT STOCKS WELL

RULE 3 - AS THE NUMBER OF STOCK ITEMS INCREASES, SET THEM OUT IN THEIR SEPARATE GROUPS

Dresses must be stored by type of dress, model and size. The sizes must be clearly marked. Items such as cans of paint must be set out by maker, size, if there is more than one size (1/2 litre, 1 litre, 2 litres, etc.), and colour.

Small items - screws, nuts, washers, fuses and so on-may be kept in small boxes, one for each article and size. The name must be marked on each box (e.g. Brass screw, 4 mm x 30 mm). The boxes must be stored by item and size. Whatever stock control system you use, your shelves and stock room must be kept in order.

If you have only a few different stock items, you will not need written stock records. You can simply look at the separate groups, count them and see whether you need to reorder some items, or whether you have overstocked some goods which are not selling.

SET OUT STOCKS BY SIZE

RULE 4 - WHEN THE NUMBER OF STOCK ITEMS GROWS TO MORE THAN 20, KEEP SIMPLE WRITTEN STOCK RECORDS

When you have many stock items, it takes too much time to count them. They will also be difficult to find. Write them into a book or on cards. Read the next section to find out how.

KEEP STOCK

RECORDS

Unit stock control

Manufacturers as well as service operators and retailers can use a unit stock control system. This type of stock control is called unit stock control because it shows the number of units or articles which are in stock. Under this system you have a card for each of the different types of stock.

Here is an example of a stock card for retailers. The system works in exactly the same way for a manufacturer or service operator.

Each time you buy or sell batteries, you enter the date and particulars on the card.

The Balance column is adjusted to show how many batteries are still in stock.

When do you reorder your batteries? To find out, you must know-

· how many batteries you sell every week or every month;

· how long it takes you to get delivery of batteries.

You find from the above stock card that you sell 40 batteries each week. Your supplier can deliver the batteries one week after you have given him your order. Therefore, you should order when your stock is 100 or below. This gives you 40 in hand for the week's delay and 60 more in case they do not come on time or you sell more than 40 in the next week. So 100 is your reorder level.

REORDER WHEN 100

LEFT

Value stock control

If you are a retail trader you can use a simple stock control system which tells you the total value of all the goods which you have in stock rather than the number of units.

In all shops, goods are purchased at a lower price-the cost price-and resold at a higher price-the selling price. When you keep stock records, you want to know either how much your business would get if all the goods than are in stock were sold, or how much has been paid by you in total for all the goods in stock.

The easiest method is to record the value of all your stock at selling price. It is easier to use selling prices since they are marked on the goods which customers buy and they are used when sales are recorded.

The easiest way to record your stock is to use a stock control book as below:

|

Stock control book | |||||

|

Month |

January 1986 |

| |

| |

|

Date |

Particulars |

Increase in stock (value in) |

Decrease in stock (value out) |

Balance stock in hand (value) | |

|

1 Jan. |

Opening stock |

|

|

43,250 | |

|

2 Jan. |

Sales |

|

3,200 |

40,050 | |

|

3 Jan. |

Purchase |

|

|

| |

|

| |

Goods Ltd. |

3,000 |

|

43,050 |

The entries in the book are the same as the entries on the stock cards above, except for the fact that the entries are made in value instead of units.

Some special situations

Some items, such as wooden planks, steel rods, sheets of metal and bolts of cloth, are difficult to count quickly and easily. In these cases, the solution is to have a bin card. This card contains all the information needed about the item, and is kept with each item on the rack, shelf and so on.

Every movement, in or out, of the item is recorded on the card. When the reorder level is approached, you reorder the item. Note the hole at the top-it can be tied to a nail or drawer handle.

USE BIN CARDS FOR SPECIAL

ITEMS

|

No. 62 0 |

BIN CARD | ||

|

Date |

In |

Out |

In stock |

|

13 Oct. |

| |

3,200 |

|

14 Oct. |

|

1,000 |

2,200 |

|

18 Oct. |

|

700 |

1,500 reorder! |

|

22 Oct. |

5,000 | |

6,500 |

Small items, such as nails, washers and so on, are very tedious to count. One way of handling them is to count out or weigh out the reorder level quantity into a paper or plastic bag, and put the bag at the back of the drawer, shelf or bin. When you have to open the bag to serve a customer, you know it is time to reorder.

Slow-moving stocks take up space that you may want for goods which sell well. Try to sell them off as special offers at reduced prices.

WHEN YOU OPEN THE BAG:

REORDER!

If they are very old, sell them off at cost price or give them away.

Figure

Handling cash

You must know exactly how much cash you take in and how much you give out - and how you spend it.

Figure

A simple way to control your cash is as follows:

1. Count your amount of money when the business opens in the morning. Whenever you take in cash, put it in the drawer. Each time you pay out cash, write out a cash voucher.

2. Count the amount of cash again at the end of the business day.

3. The difference between the amount in the morning and the amount in the evening is called your net takings.

4. Add up your cash vouchers. This gives the total cash paid out during the day. Remember that this cash has been taken from the cash drawer, and so must be added on to the net takings to show the total cash which has come into the business during the day.

Figure

|

Vouchers |

70 |

|

plus: Net takings |

200 |

|

Total cash in |

|

|

from sales |

|

|

during the day |

270 |

5. Add the total of the vouchers to your net takings. This gives you the total cash which has come in from sales during the day.

How to control cash

It is easier to control the cash coming in and the cash going out if you write down the details of every sale and payment in a cash book.

If you have a bank account, you can also add columns for Bank in and Bank out.

Your cash book can look as follows:

|

Date |

Details |

Cash in |

Cash out |

Bank in |

Bank out |

|

1 Mar. |

Cash at start |

100 |

|

|

|

|

1 Mar. |

Cash sale |

150 |

|

|

|

|

1 Mar. |

Toilet rolls |

|

20 |

|

|

|

1 Mar. |

Typewriter ribbons |

|

15 |

|

|

|

1 Mar. |

Cash sale |

120 |

|

|

|

|

1 Mar. |

To bank |

|

35 |

35 |

|

|

|

|

370 |

70 |

35 |

|

|

Less: |

Cash at start |

100 |

|

|

|

|

|

Total money |

|

|

|

|

|

|

from sales |

270 |

|

|

|

|

Less: |

Cash out |

70 |

|

|

|

|

|

Net cash in |

200 |

|

|

|

The cash register

If you area retail trader you should keep a cash register which you or an honest employee or member of your own family operates. One person should be in charge of both cash going out of and cash coming into the cash register. The business cash must be kept separate from your own cash and the cash of members of your family.

By keeping the cash register paper rolls, you can see what you take in and give out every day, week, month or year. It is good to see how money comes in and is paid out over a long time because business may change from day to day. One day it may be very good, the next day bad. Compare your business result of this month with that of last month.

KEEP THE CASH REGISTER PAPER

ROLLS

The rules of cash control

1. Do not allow members of the family to take cash from the business unless it is their wage, it is given by you and they sign a receipt for it.

Figure

2. Pay yourself and each member of the family working in the business regular wages which you can charge to the business like those of your other employees. This can help you to have more control over the outflow of your cash.

3. Decide on how much you can draw each week as a salary for yourself, but keep it low. Remember, you must also put aside money to buy stocks, pay wages, replace old machinery, pay taxes and so on. You must also have something left over in reserve in case business is bad or you want to make it bigger. This is the only way you can build up capital and improve your business.

Figure

4. If you or a member of your family takes goods from the shop or the business-a can of food or a piece of clothing, for example-put the money into the cash box.

Figure

5. Make sure that you have enough money in the bank to meet the normal needs of the business.

Figure

Good bookkeeping

REMEMBER: TAKE CARE OF YOUR CASH!

As your business grows and you buy and sell more of different goods, you need more information from your accounts. Therefore bookkeeping is important. To know more about it, read the Bookkeeping section of the Handbook. If you want to set up a bookkeeping system, you may get help from your local Small Business Centre or you may hire someone. This means that you must save all your bills, invoices, cash register rolls and other papers about money to give him when he comes.

And last, but not least, once again: Keep your own and your family's hands out of the business cash!

KEEP ALL HANDS OUT OF THE CASH

DRAWER!

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Improve Your Business: Handbook (ILO, 1986, 144 p.)

2. MANUFACTURING AND SERVICE OPERATING

Manufacturing

Manufacturing means processing and/or assembling raw materials and sometimes parts to make them into products, using workers (labour), machines, tools and power.

The raw materials (wood, steel, cloth, chemicals, etc.) and the parts (handles, nails, screws, wire, thread, etc.), as well as the labour and the power, are called inputs because they are put into the making of the products.

INPUTS

MANUFACTURING

OUTPUTS

Products are the goods which are manufactured or produced in a workshop or factory.

The quantities of products produced by a business during a period of time are called the outputs.

The stages of manufacturing

The stages of manufacturing always follow one another in the same order, whatever the products may be.

STAGE 1 - STORING

The materials and parts which have been bought arrive in the raw material store. They are checked and stored till needed.

Figure

STAGE 2 - PROCESSING

The raw materials are processed, for example by cutting, sawing, machining or sewing.

Figure

STAGE 3 - ASSEMBLING

The parts are put together to make a product (i.e. assembly takes place). Where the product is simple - flour, cotton yarn or steel bars - assembly does not take place.

Figure

STAGE 4 - FINISHING

Finishing takes place. This includes, for example, painting, polishing, washing, dyeing or glueing.

Figure

STAGE 5 - INSPECTION

Inspection takes place to check that the product has been made correctly and is ready to be sent to the customer. This is a check for quality.

Figure

STAGE 6 - PACKING

The product is packed, ready to be sent to the customer.

Figure

Each stage of manufacturing involves costs. Some of these costs are unavoidable, as you need raw materials, labour and energy to manufacture your product. But in manufacturing businesses the amount of money spent on these items is often greater than it should be. This leads to high costs. The main causes of these high costs are:

· waste of raw materials;

· waste of workers' time;

· waste of machine time;

· waste by tying up too much working capital.

It is important that your goods are produced with the smallest possible waste. Waste adds to the cost of the product and reduces the possible profit.

The cheaper you can produce, the cheaper you can sell, so that:

· more people buy your goods; and

· you are more able to compete with other manufacturers.

Figure

Cut your costs by reducing your waste, and you will get a bigger profit.

Figure

Cutting the cost of raw materials

The cost of materials can be made less by-

· Good buying. This is even more important in manufacturing than in retail trade. Price is not everything. Cheap materials may mean more material that cannot be used because it is faulty and must be thrown away, so that the material you can use becomes dearer.

· Cutting down waste. In woodworking, sheet metalworking, shoemaking, dressmaking and tailoring, among other trades, skilled cutting can make great savings as against bad cutting.

· Cutting down spoiled work. This must then be thrown away or sold off cheaply. When work must be scrapped, you lose not only the cost of machine time but also the money which you would make if the product were sold.

BAD CUTTING GIVES ONE SHIRT BUT

GOOD CUTTING GIVES TWO SHIRTS

Good training of workers, good tools and working conditions, good wages and strong supervision will cut down spoiled work.

Cutting labour costs

This will not be done by cutting wages. It must be done by cutting down the amount of time which a worker wastes when he is doing a job. The costs of labour are calculated on the basis of the time spent by a worker to do a certain piece of work. The less the time spent, the less the cost.

How is time wasted by workers?

· By making workers walk, and carry materials through the workshop further than they need, because machines, workplaces and stores are badly placed.· By giving workers bad workplaces, which are untidy, difficult to work at and badly lit, and by giving them unsuitable or worn-out tools for the job to be done.

TIME IS WASTED BY: WALKING TOO MUCH POOR WORKPLACES BAD TOOLS

WORKSHOP LAYOUT

Workshop layout is the way in which machines, workbenches and storage places in a workshop are placed in relation to each other.

Good layout means that the product travels and is handled as little as possible between stages of manufacture, and that people walk as little as possible. Bad layout means that the product travels and is handled too much during its manufacture, and that people walk too much.

Bad layout costs you money because products take longer to make than they need to take. To get the same output, you need:

· more workers;

· more handling equipment;

· more space (bigger factory buildings).

All these things mean more costs.

BAD WORKSHOP LAYOUT COSTS YOU MONEY AND CUTS PROFITS

Figure

So your profits are less and you may lose orders to companies which do things better. It is your money you are wasting.

With bad layout, the product goes back and forward between processes. This uses more labour and more trucks, makes delays at machines and makes work difficult to find. Space is taken up in a bad way.

Good layout is most important when the product or materials used are heavy or big, as in sheet metalworking and woodworking. In wood machining the machines cut very fast. If the machines are in the right order there is little delay between the stages of manufacturing. The time spent moving big and heavy pieces of wood from the store to the shop, round the shop and on to the machines may be five or ten times as long as the cutting time.

If you are in a trade where heavy materials and work must be handled, think how you can make the handling time less.

You cannot always make the best layout, for example in an old factory building; but one thing you can do is to be tidy.

· Keep your workshops tidy-put everything in its right place so that it is easy to find.

· Keep your gangways clear and tidy.

· Tidiness saves time and is safe.

GOOD WORKSHOP LAYOUT SAVES YOU MONEY AND INCREASES PROFITS

Figure

WORKPLACE LAYOUT

Workplace layout is the way in which tools and materials are laid out and the finished work is stored at the place where the work is done.

The workplace which you see in the picture on the left below can be seen in thousands of small workshops all over the world. What a mess!

Figure

Figure

If you do not believe it, go and look at some small (and big) workshops near you. Finished work is mixed with pieces to be assembled. The tools are in the wrong places. The wire is tangled. The workers have to look for everything they want. They will take a much longer time to make one assembly than workers who sit at a neat workplace.

Now look at the picture on the right above. This is a good workplace layout. The worker has a chair to sit on, so he or she will be less tired. The pieces to be assembled are always in the same place so that they can be picked up without looking. The wire is on a reel. The welding nozzle is on a hook close to the worker's right hand. The screwdriver is hanging on a spring on the same side, easy to reach and use. The finished assemblies are put into a box on the left, ready to take away.

GOOD WORKPLACE LAYOUT MEANS EVERYTHING IN ITS RIGHT PLACE

|

Remember: · Good workplace layout is important where products are small and light and produced from many parts in large quantities. · Work study will help you make better layouts and save money. Ask about it at your Small Business Centre or Management Centre. |

SAFETY

Workshop safety is extremely important both to you and your workers. As the owner/manager you are responsible for injuries and illness caused by poor safety standards or ignorance of risks that you and your workers are exposed to. Safety means not only preventing accidents but also doing something about bad working conditions like very loud noise or poor light, dangerous liquids or gases and so forth.

Remember that if something happens because you have not paid enough attention to workshop safety, you are causing other people pain and distress and you might end up paying for damages for the rest of your life.

There are a number of measures you can take in order to safeguard the health and security of your workers:

· Organise the work so that the different stages can be carried out smoothly and without pressure. Many accidents occur when people are moving in workshops from one workplace to another, or when they are collecting raw materials or carrying away finished goods.· Give your workers detailed instructions on how to use machines, tools and chemicals before they start working. Make sure that the safety equipment that you provide is also used by your workers. Never let a worker without proper training repair or adjust machines.

· Avoid having visitors walking around in the workshop on their own. People who are unfamiliar with your business might not have the necessary respect for tools and machines.

· Always think about safety factors when you are making investments in new machines. Ask for written instructions on how to use them.

AVOID ACCIDENTS BY:

GOOD WORK ORGANISATION

TRAINING

SAFE MACHINERY AND EQUIPMENT

Cutting the cost of machines

CUTTING MACHINE TIME

Machines cost money, sometimes a lot of money. When you have paid money for a machine you must use it as well as possible. In many workshops, machines spend more time stopped than they do working. Why?

Because-

· the workers operating the machines must spend time fetching material from the store and taking away finished work;· the next job is not ready when the earlier job is finished, and the worker and machine are waiting for work;

· the machines break down.

In addition to these causes, machines are often not working at their correct speeds, tools are not properly sharpened and the workers are not trained to use the machines well.

Before beginning work with a machine, make sure that it is working as well as possible and that the worker really knows how to use it well.

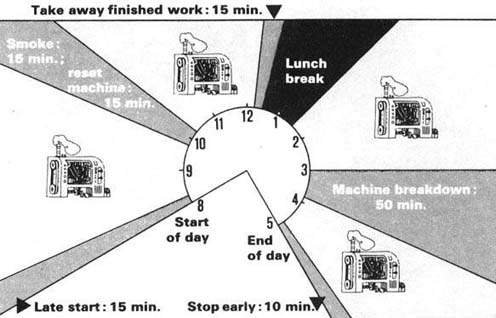

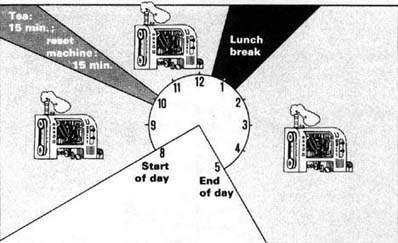

Let us look at an example of how time can be lost in working a machine during a working day of eight hours from 8 a.m. to 5 p.m. plus a one-hour meal break from 12.30 p.m. to 1.30 p.m.

MACHINES COST MONEY-USE THEM WELL!

Look at clock no. 1. The time during which the machine is producing work is shown in light grey. The time when the machine is stopped during the working day is shown in black. Clock no. 1. shows how you could operate your machine in the best way. There are no stoppages between 8 a.m. and 5 p.m. apart from the lunch break.

Clock no. 1

The machine worked for eight hours, with no stoppages.

Now look at clock no. 2 on the opposite page. There are five dark grey pieces in clock no. 2.

Each dark grey piece shows the time when the machine was stopped, apart from at the lunch break, which is shown in black.

Clock no. 2

Clock no. 2 shows that you did not operate your machine in a good way. There were many stoppages for the following reasons:

|

· The worker is late |

15 min. lost (8 a-m.-8.15a.m.) |

|

· The machine is reset |

15 min. lost (9.45a.m.-10.00a.m.) |

|

· The worker has a smoke |

15 min. lost (10.00a.m.-10.15a.m.) |

|

· The worker carries away finished goods |

15 min. lost (12.15 p-m.-12.30 p.m.) |

|

· The machine breaks down |

50 min. lost (3.00 p.m.-3.50 p.m.) |

|

· The worker stopped early Total time machine stopped: |

10 min. lost (4.50 p-m.-5.00 p.m.) 120 min. = 2 hr. |

Due to the stoppages, the actual working time of the machine was reduced from eight hours to six hours, as below:

|

|

Total working time of machine |

8 hr. (480 min.) |

|

Less: |

Machine stopped |

2 hr. (120 min.) |

|

Gives: |

Working time of machine |

6hr. (360 min.) |

In other words, the machine was stopped for one-quarter (i.e. 25 per cent) of its total working time.

Now look at clock no. 3 on the next page and compare it with clock no. 2.

In clock no. 3 there is only one dark grey piece left.

Clock no. 3

Let us see what has happened:

|

· The worker starts on time |

15 min. saved |

|

· The worker does not have to carry away finished goods |

15 min. saved |

|

· The machine does not break down |

50 min. saved |

|

· The worker does not stop work early |

10 min. saved |

|

Total machine time saved: |

90 min. =1 1/2 hr. |

One-and-a-half hours of working time were saved due to management improvements. The actual working time of the machine was increased from six hours to seven-and-a-half hours, as shown below:

|

|

Total working time of machine |

8 hr. (480 min.) |

|

Less: |

Machine stopped |

1/2 hr. (30 min.) |

|

Gives: |

Actual working time of machine |

7 1/2 hr. (450 min.) |

In other words, the machine was stopped for only one-sixteenth (6 per cent) of its total working time.

MACHINE MAINTENANCE

Machine maintenance is looking after machines and equipment, including vehicles, by oiling, greasing, checking that they are in good working order, replacing worn parts before they break, and checking electrical parts and wiring.

To work well, maintenance must be done regularly: oiling and greasing, say, once a week; checking for worn parts once a month; and checking the electrical parts every three months. The more a machine costs, the more important is good maintenance.

REGULAR MAINTENANCE PREVENTS

BREAKDOWNS

If you must stop a machine for a long time to do a good job on it, plan to stop it when you think it is best. It is better to stop a machine when you want to do it than to have it break down and stop when it is doing important work. By good maintenance, you avoid stoppages due to breakdowns.

HANDLING ON AND OFF MACHINES

We said earlier that in some trades it takes much longer to bring the material to the machine and to put it on the machine than it does to cut or work the material. It may also take longer to take the work off the machine. This is true of woodworking, where big logs of wood are difficult to handle. The same can be true of sheet metalworking, because the sheets are large and heavy. It can also be true of dressmaking when the dress or shirt is nearly finished.

HANDLING BY HAND-SLOW

If you can only make the handling time in each operation smaller, you can make your output bigger. Many business people spend a lot of money on highspeed machines and lose most of the bigger output because they do not cut their handling time.

HANDLING BY BARROW-FAST

If you are in a trade where heavy materials and work must be handled, think how you can make the handling time less and get advice.

Cutting the cost of working capital tied up

Cash is a most important asset used in running your business. Cash enables you to buy raw materials, pay your workers and office staff, and pay for all the other expenses such as rent, insurance, telephone and so on.

Cash flows into your business from five different sources:

· from your own savings;

· from loans which you obtain from a bank;

· from relatives or friends;

· from sales on credit; and

· from cash sales.

At the time you started your business, your cash came only from your own savings and maybe from a loan. You used this cash first of all to buy machines, tools, equipment and other assets. All these are called fixed assets, because they are fixed in your business for a very long time. This means that your money is tied up in them for a very long time.

FIXED ASSETS

The rest of the cash, which you did not spend on fixed assets, is called working capital. You used it to buy raw materials and parts for production and to pay the wages and salaries and other expenses during the first two months or so of production. From then on you have received cash back from the finished goods which you make and sell.

WORKING CAPITAL

You normally receive your cash in two ways:

· quickly when you make cash sales; and

· more slowly when you make sales on credit, since people take a long time to pay.

A CREDIT SALE MEANS CASH

LATER

A CASH SALE MEANS CASH NOW

The cash which you receive from your sales is your new working capital. This is slightly more than the cash you spent on making the goods which you sold, because you made a profit. You now use this new working capital to buy more new materials and parts, which you convert into more finished goods and, when you sell these, this will give you even more cash (working capital) back than you spent before. Now you can see why this cash is called working capital: it works for you; it helps you to earn a profit.

Naturally, the faster you get your cash back after you spend it, the faster you make a profit and the faster your cash (working capital) increases. Therefore the raw materials which you purchased should be processed and turned into finished goods as quickly as possible, so that they can be sold and the money from sales flows back into your business.

WORKING CAPITAL

¯

BUYING

MATERIALS V

¯

MANUFACTURING OF GOODS

V

¯

SELLING OF GOODS V

¯

MORE WORKING CAPITAL

It is very bad if your materials are held up in each section of your workshop for a long time. The more stock and material are lying in your workshop, the more working capital is tied up in them.

You should try to organise your production in such a way that you manufacture with a minimum of materials and semi-finished goods held up in your workshop.

Look at the example below, where a lot of working capital is tied up in stock in the workshop.

|

1. Raw materials store |

| |

|

Working capital tied up in raw materials: |

Working capital tied up | |

|

10,000 |

10.000 |

|

|

2. Processing section |

| |

|

Working capital tied up in partly processed goods: 5,000 |

+ 5,000 |

|

|

3. Assembly section |

| |

|

Working capital tied up in partly assembled goods: 5,000 |

+ 5.000 |

|

|

4. Finishing section |

| |

|

Working capital tied up in partly finished goods: 2,500 |

+ 2,500 |

|

|

5. Inspection section |

| |

|

Working capital tied up in goods waiting for inspection: 2,500 |

+ 2,500 |

|

|

6. Finished goods store |

| |

|

Working capital tied up in finished goods lying in store: 5,000 |

+ 5,000 |

|

|

Total cash (working capital) tied up in stock: 30,000 |

= 30,000 | |

The more stock you hold, the more cash is tied up and the less cash you have in hand. Now look at the results you can obtain after making some improvements.

|

1. Raw materials store |

Working capital tied up after improvements | |

|

Working capital tied up in raw materials: 5,000 |

5,000 |

|

|

2. Processing section | | |

|

Working capital tied up in partly processed goods: 2,500 |

+ 2,500 |

|

|

3. Assembly section | | |

|

Working capital tied up in partly assembled goods: 2,500 |

+ 2,500 |

|

|

4. Finishing section |

| |

|

Working capital tied up in partly finished goods: 1,250 |

+ 1,250 |

|

|

5. Inspection section | | |

|

Working capital tied up in goods waiting for inspection: 1,250 |

+ 1,250 |

|

|

6. Finished goods store |

| |

|

Working capital tied up in finished goods lying in store: 2,500 |

+ 2,500 |

|

|

Total cash (working capital) tied up in stock: 15,000 |

= 15,000 |

|

In the example above, you can reduce the money tied up in stock by moving the stock faster through the factory. You can do this in many ways. We have already talked about some improvements you can make:

· improved workshop layout;

· improved workplace layout;

· better machine maintenance;

· quicker loading and unloading of machines;

· shorter machine time.

You can also reduce the money tied up by:

· quick delivery of your finished goods to the customers after you have sold the goods, and getting as much of the payment in ready cash as quickly as possible;· making sure that the customers to whom you sell on credit pay you cash strictly within two months after the delivery of the goods.

REDUCE WORKING CAPITAL TIED UP BY:

HOLDING LESS STOCK

DELIVERING GOODS

QUICKLY

LIMITING CREDIT SALES

The saving in cash is: 30,000 - 15,000 = 15,000. You now produce the same output with much less working capital tied up. With all this extra cash in hand, you may be able to finance all your purchases and expenses without having to go for a loan. You may even have some money to make the business bigger.

Increase your profit by using your working capital in a better way - Do not tie it up!

Figure

REMEMBER:

GOODS OUT FAST-

CASH IN

FAST

Service operating

Service industries do not usually produce goods, but they render services to the public or some section of the public.

There are generally more small businesses in the service sector of industry than in the manufacturing sector. Service industries include garages and other repair workshops, television and radio repairs, laundries, dry-cleaning, passenger and goods transport services, hotels, restaurants and bars.

Business people in the service sector may think that the section of this book on manufacturing is of no use to them. It is true that some services, for example garages and repair workshops in general, and laundries, come very close to manufacturing industries, while others, such as bars, may seem very different. Although service industries do not generally use raw materials to make a product (although restaurants do), they use spare parts for repairs, fuel, heating, electricity and water for washing, cleaning, running vehicles and so on. They also use labour to repair, drive, clean, cook or serve, and equipment such as tools or vehicles, buildings and land just like manufacturing businesses.

To operate a service efficiently, we must use the same means as we use in manufacturing industry. The first step is to know your costs.

A SERVICE BUSINESS USES

SPARE PARTS

MATERIALS

LABOUR

TOOLS

A BUILDING

JUST LIKE

A MANUFACTURING

BUSINESS

The same methods that are used in manufacturing to cut out waste and make sure of good use of workers' time and of machines can be used in operating services. Safety is also as important in a service industry as it is in manufacturing. Read the part of this section on " Manufacturing " carefully and see what you can apply in your service business.

Know your costs

Knowing the costs of different items makes it possible to attack the biggest item of cost first. In manufacturing firms, this is generally the direct material cost but in service industries it may be direct labour, fuel or some other cost. To cut these costs you can use the same methods described for manufacturing:

ATTACK YOUR BIGGEST COST ITEM FIRST

· better buying and cutting down waste of materials, including fuel, power and energy;

CUT DOWN WASTE OF ENERGY

· reducing labour costs by better layout, working methods and tools, and by cutting ineffective time;

IMPROVE WORKPLACE LAYOUT

· improving the use of equipment, including vehicles, by better planning, including planned maintenance.

IMPROVE

MAINTENANCE

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Improve Your Business: Handbook (ILO, 1986, 144 p.)

3. BOOKKEEPING

Bookkeeping is writing down all the transactions arising from your business activities which can be expressed in money.

To run your business well you must know what money you have received, how much money you have spent and, most important of all, how you spent it. A bookkeeping system can provide you with that information. Good information removes the guesswork from business.

This section provides you with all the information you need to set up a simple, useful system of keeping records.

The books used for keeping records consist of a ledger and subsidiary books.

The ledger is the general book in which you enter almost all the figures arising from your business activities.

The subsidiary books are used to record information which will help you to remember important things about your business, e.g. the bills you have to pay or the wages you pay. The number of subsidiary books varies depending on the size and the kind of business you are in.

THE LEDGER IS THE MAIN BOOK

THE SUBSIDIARY BOOKS HELP YOU TO

REMEMBER IMPORTANT

THINGS

The ledger

Every business transaction consists of two parts, one part that gives and one part that receives-one part that goes out of the business and in exchange one part that comes into the business. For example, if you sell goods, goods go out and cash comes in. Therefore you must make two entries for each business transaction.

If you sell goods, the goods go out of the business. Therefore you make an "Out" entry in the ledger. In place of what has gone out of the business, something else goes in. In this particular case money comes in for what is sold. You also make the "In" entry in the ledger.

Figure

REMEMBER: ALWAYS ONE IN AND ONE OUT ENTRY FOR EACH TRANSACTION

A ledger consists of a number of accounts. An account is a column in the ledger that has been given a specific name, e.g. Cash, Bank, Sales and so on. In some ledgers a whole page is used as one account. Here we will use the type of ledger where a page is divided into several columns, each column regarded as one account.

|

CASH |

BANK |

|

CASH |

BANK |

SALES |

RAW MAT.* | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| | | |

|

|

|

|

|

|

page 1 |

|

|

page 2 |

|

|

|

|

|

|

| | | |

|

|

|

|

|

|

One account on each page |

|

Several accounts on each page |

* RAW MAT. = raw materials | |||||||||||||||

STEP 1

The carpenter sells a chair to a customer. We need two accounts to record that transaction: one account to record the money that goes into the business (the Cash account) and one account to record the value of the chair that goes out of the business (the Sales account).

Our ledger now has two accounts, one called "Cash" and one called "Sales". The Cash account has three columns. One column is marked "In". This is used for entries when money comes into the business. The next column is marked "Out". This is used when money goes out of the business. The third column is for the Balance, or "Bal." for short.

|

|

|

|

CASH |

|

SALES |

|

| ||||||

|

|

|

|

In |

Out |

Bal. |

|

|

|

In |

Out |

|

|

|

| | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Look at the Cash account below.

Suppose the carpenter gets 100 NU for the chair. Assume that there was 300 NU in the cash box before the sale of the chair. The entries step by step will be as follows:

|

CASH |

CASH |

|

|

In |

Out |

Bal. |

|

|

|

300 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 Before the sale of the chair. The balance in the cash box is 300 NU

|

CASH | ||

|

In |

Out |

Bal. |

|

|

|

300 |

|

|

|

|

|

100 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2 100 NU has gone into the business as a result of the sale of the chair

|

CASH | ||

|

In |

Out |

Bal. |

|

|

|

300 |

|

|

|

|

|

100 |

|

400 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 The addition of 100 NU to the 300 NU already in the cash box makes 400 NU

The Cash account and the account showing what we have in our bank account are the only accounts where this "Balance" column is used. All other accounts are divided into two columns, one "In" and one "Out". The reason why there is a Balance column in the Cash and the Bank accounts is that we want to know instantly how much money is present in the business.

STEP 2

Let us enter the sale of the chair in the Sales account. The value of the chair was 100 NU and the chair has now gone out of the business. The entry of 100 NU will be made in the "Out" column of the Sales account, and 100 NU goes into the "In "column of the Cash account.

In the ledger below we have now entered all the figures arising from the sale of the chair.

|

SALES |

|

|

|

|

CASH |

|

SALES | ||||||

|

In |

Out |

|

|

|

|

In |

Out |

Bal. |

|

|

|

In |

Out |

|

|

| | | | |

|

|

300 |

|

|

|

|

|

|

|

100 |

® |

|

|

|

100 |

|

400 |

|

|

|

|

100 |

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| | |

|

|

|

|

|

|

|

|

|

|

There are two accounts in the ledger. We must add more accounts, but first let us look at the space to the left of the Cash account. There we make some remarks concerning each transaction. We write the date of the sale and also write that it was a chair that was sold.

Finally, we shall give this transaction an identification number (Id.no.). We also write the number on the copy of the receipt we give to the customer. We keep the copy in a file together with other vouchers related to entries in the ledger.

KEEP ALL YOUR VOUCHERS IN A

FILE

Look at the columns to the left of the cash account below:

|

DATE |

PARTICULARS |

ID.NO. |

CASH |

|

SALES |

|

| ||||||

|

|

|

|

In |

Out |

Bal. |

|

| |

In |

Out |

|

|

|

| | | |

|

|

|

| | |

|

|

|

|

|

The ledger entries are now added as shown below:

| | | | |

IN | |

OUT | | | ||||||

| | | | |

| |

| | | ||||||

| |

DATE |

PARTICULARS |

ID.NO. |

CASH |

|

SALES |

|

| ||||||

| |

MAY |

|

|

In |

Out |

Bal. | |

|

|

In |

Out |

|

|

|

| | | | |

|

|

300 |

|

|

|

|

|

|

|

|

|

|

2 |

1 CHAIR |

86 |

100 |

|

400 |

|

|

|

|

100 |

|

|

|

| |

|

|

|

|

|

| |

|

|

|

|

|

|

|

| |

|

|

|

|

|

| |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

| | |

|

|

|

| |

|

|

|

|

|

|

|

|

|

| |

|

|

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

|

| |

|

|

|

|

|

|

|

|

| |

|

| |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

| |

|

|

|

STEP 3

Let us add more accounts into our ledger.

| | | | |

OUT |

| |

IN |

| ||||||

|

| | |

|

| | |

| | ||||||

| |

DATE |

PARTICULARS |

ID.NO. |

CASH |

|

SALES |

RAW-MAT. |

| ||||||

| | | | |

In |

Out |

Bal. |

| |

|

In |

Out |

In Out |

| |

| |

WAY |

|

|

|

|

500 |

| |

|

|

|

|

|

|

| |

2. |

1 CHAIR |

86 |

100 |

|

400 |

| | |

|

100 |

|

|

|

|

|

4 |

WOOD |

87 |

|

150 |

250 |

|

|

|

|

|

150 |

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The carpenter has to buy raw materials. A Raw material account is needed. In the ledger above this account is added and we also have the following example entered: the carpenter buys wood and pays 150 NU cash to the supplier.

The ledger tells us that on 4 May wood was bought at a price of 150 NU. The cash was paid out, and after the payment 250 NU remains in the cash box. On the receipt given by the supplier of the wood the carpenter has written "87". The receipt can easily be found in the file where all the numbered vouchers are kept.

NUMBER ALL YOUR VOUCHERS

STEP 4

We must pay wages to the workers. An account called "Wages" is added.

The carpenter pays four employees 50 NU each in cash, so 200 NU is taken from the cash box.

Look at the entry. Wages have been paid on 6 May. In total 200 NU is paid and the money is taken from the cash box (i.e. it is put into the "Out" column of the Cash account). We have 50 NU remaining in the cash box.

| | | | |

OUT |

IN |

| |

IN |

OUT |

| | |

| ||||||||||||

|

| | |

|

|

| | |

|

| | | | | ||||||||||||

| |

DATE |

PARTICULARS |

ID.NO. |

CASH |

BANK |

SALES |

RAW MAT. |

WAGES |

LOANS |

EQUIPMENT |

INTEREST |

DRAWINGS |

OTHERS | ||||||||||||

|

| | | |

In |

Out |

Bal. |

In |

Out |

Bal. |

In |

Out |

In |

Out |

In |

Out |

In |

Out |

In |

Out |

In |

Out |

In |

Out |

In |

Out |

| |

WAY |

|

|

|

|

300 |

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

2 |

1 CHAIR |

88 |

100 |

|

400 |

|

|

|

|

100 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

4 |

WOOD |

87 |

|

150 |

250 |

|

|

|

|

|

150 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

STEP 4 |

6 |

WAGES |

88 |

|

200 |

50 |

|

|

|

|

|

|

|

200 |

|

|

|

|

|

|

|

|

|

|

|

|

STEP 5 |

7 |

LOAN |

89 |

|

|

|

6,000 |

|

6,000 |

|

|

|

|

|

|

|

6,000 |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The reason why wages are entered in the " In " column of the Wages account is that the money represents the time the workers put into the business.