|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

International Edition

Written by Mats Borgenvall, H�kan Jarskog,

Barbara

Murray and Cecilia Karlstedt

This edition adapted by H�kan Jarskog

|

|

INTERNATIONAL LABOUR OFFICE |

Copyright © International Labour Organization 1999

First published 1999

Publications of the International Labour Office enjoy copyright under Protocol 2 of the Universal Copyright Convention. Nevertheless, short excerpts from them may be reproduced without authorization, on condition that the source is indicated. For rights of reproduction or translation, application should be made to the Publications Bureau (Rights and Permissions), International Labour Office, CH-1211 Geneva 22, Switzerland. The International Labour Office welcomes such applications.

Libraries, institutions and other users registered in the United Kingdom with the Copyright Licensing Agency, 90 Tottenham Court Road, London W1P 9HE (Fax +44 171 436 3986), the United States with the Copyright Clearance Center, 222 Rosewood Drive, Danvers, MA 01923 (Fax +1 508 750 4470), or in other countries in accordance with associated Reproduction Rights Organizations, may make photocopies in accordance with the licences issued to them for this purpose.

|

Borgenvall, Mats; Jarskog, H�kan; Murray, Barbara; Karlstedt,

Cecilia ILO Cataloguing in Publication Data |

The designations employed in ILO publications which are in conformity with United Nations practice, and the presentation of the materials therein, do not imply the expression of any opinion whatsoever on the part of the International Labour Office concerning the legal status of any country, area or territory or of its authorities, concerning the delimitation of its frontiers.

The responsibility for opinions expressed in signed articles, studies and other contributions rests solely with their authors, and publication does not constitute an endorsement by the International Labour Office of the opinions expressed in them.

Reference to names of firms and commercial products and processes does not imply their endorsement by the International Labour Office, and failure to mention a particular firm, commercial product or process is not a sign of disapproval.

ILO publications can be obtained through major booksellers or ILO local offices in many countries, or direct from ILO Publications, International Labour Office, CH-1211 Geneva 22, Switzerland. Catalogues or lists of new publications are available free of charge from the above address.

Design, illustrations and typesetting by Robert Silverman Design, Brooklyn, New York, USA.

Printed in Switzerland

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

ABOUT START AND IMPROVE YOUR BUSINESS

Improve Your Business (IYB) is an integral part of the ILO’s Start and Improve Your Business (SIYB) package, which is part of the International Small Enterprise Programme (ISEP). ISEP strives to assist member countries of the ILO in their efforts to meet the global employment challenge by creating sustainable quality jobs in the small-scale private enterprise sector.

At a time when the employment capacities of the agricultural, public and large-scale enterprise sectors have reached their limit in many countries, it is clear that most future jobs will need to be created in the small-scale enterprise sector. The SIYB programme has been designed to provide a sustainable and cost-effective method to reach substantial numbers of small-scale entrepreneurs and provide them with the practical management skills needed in a competitive environment for profitability and growth.

SIYB is a system of interrelated training packages and support materials for small-scale entrepreneurs with limited previous exposure to management training. The programme provides individuals and institutions with a comprehensive set of materials, aimed at a variety of target groups. It deals with various topics related to small-enterprise development, such as training, business counselling, monitoring and evaluation and networking. Small-enterprise development institutions in more than 70 countries worldwide have used the SIYB programme.

More information about how the ILO can assist with the adaptation and implementation of the SIYB training programme can be obtained from any local ILO office or from:

INTERNATIONAL LABOUR OFFICE

Entrepreneurship and Management Development Branch

CH-1211 Geneva 22

Switzerland

Fax No: +41 22 799 79 78

E-mail: entreprise@ilo.org

Website: https://www.ilo.org/public/english/65entrep/siyb/index.htm

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

THE INTERNATIONAL LABOUR ORGANIZATION

The International Labour Organization was founded in 1919 to promote social justice and, thereby, to contribute to universal and lasting peace. Its tripartite structure is unique among agencies affiliated to the United Nations; the ILO’s Governing Body includes representatives of government and of employers’ and workers’ organizations. These three constituencies are active participants in regional and other meetings sponsored by the ILO, as well as in the International Labour Conference - a world forum which meets annually to discuss social and labour questions.

Over the years, the ILO has issued for adoption by member States a widely respected code of international labour Conventions and Recommendations on freedom of association, employment, social policy, conditions of work, social security, industrial relations and labour administration, among others.

The ILO provides expert advice and technical assistance to member States through a network of offices and multidisciplinary teams in over 40 countries. This assistance takes the form of labour rights and industrial relations counselling, employment promotion, training in small business development, project management, advice on social security, workplace safety and working conditions, the compiling and dissemination of labour statistics, and workers’ education.

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

ILO PUBLICATIONS

The International Labour Office is the Organization’s secretariat, research body and publishing house. The Publications Bureau produces and distributes material on major social and economic trends. It publishes policy statements on issues affecting labour around the world, reference works, technical guides, research-based books and monographs, codes of practice on safety and health prepared by experts, and training and workers’ education manuals. It also produces the International Labour Review in English, French and Spanish, which publishes the results of original research, perspectives on emerging issues, and book reviews.

Catalogues and lists of new publications are available free of charge from ILO Publications, International Labour Office, CH-1211 Geneva 22, Switzerland.

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

FOREWORD

At a time when the public and large-scale enterprise sectors’ abilities to create new employment have reached their limit in many countries, it is clear that most future jobs will be created in small-scale enterprises.

Few business management publications are simple and clear enough to be understood easily by people who have not been exposed to business training but which can still communicate the basic management skills required by entrepreneurs if they are to run small businesses successfully and to be competitive. This book is an attempt to fill the gap.

The underlying idea of the book is that improvements can best come from active and creative thinking by entrepreneurs about their own businesses. The purpose of this material is therefore to encourage such creative thinking and motivate entrepreneurs to take action to improve their businesses.

The book is an integral part of the “Start and Improve Your Business” (SIYB) programme which in turn is part of the ILO’s International Small Enterprise Programme. The SIYB programme has been designed to provide a sustainable and cost-effective method to reach substantial numbers of small-scale entrepreneurs and provide them with the practical management skills needed in a competitive environment for profitability and growth. The SIYB programme is progressively including principles of social concern in its business management training, thereby contributing to the enhancement of quality in employment in line with core ILO values.

The SIYB programme provides individuals and institutions with a comprehensive and interrelated set of training materials, aimed at a variety of target groups, and dealing with various topics related to small enterprise development such as training, business counselling, monitoring and evaluation, and networking. Small enterprise development institutions in more than 70 countries worldwide have used the SIYB programme.

This book can be seen as the new generation in the series of SIYB publications, and will gradually replace the IYB Handbook and Workbook published in 1986. It is accompanied by a practical Trainer’s Guide and the SIYB Game - an effective and dynamic learning tool that brings the learning points in the training programme to life. The Trainer’s Guide is adapted from a guide prepared by the Swedish International Development Cooperation Agency (SIDA) for the territories under the Palestinian Authority and is reproduced by permission.

Credit is due to the authors of the book: H�kan Jarskog, Barbara Murray, Cecilia Karlstedt, and in particular to Mats Borgenvall, who had the creative vision. H�kan Jarskog adapted this edition from the original IYB Basics edition developed in Harare by a project financed by SIDA. Acknowledgement is also due to the many consultants who have contributed to the workings and to the innumerable trainers and entrepreneurs who have provided feedback and suggestions on how to present the learning elements. Martin Clemensson has managed the overall process of transforming an idea to a publication now being used throughout the ILO’s global network.

For more information about the ILO’s activities for enterprise development, you can either visit our Website https://www.ilo.org/entreprise, contact us at the International Labour Organization, Entrepreneurship and Management Development Branch, CH-1211 Geneva 22, Switzerland, or send us a fax on +41 22 799 7978.

M. Ishida, Director

Enterprise and Cooperative

Development

Department

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

INTRODUCTION

IN THIS CHAPTER YOU WILL LEARN

How this book is organized

There are six topics in Improve Your Business Basics. Each topic helps you solve problems and improve the management of one important part of your business.

· Marketing helps you provide what your customers want

· Buying helps you buy goods, materials and equipment

· Stock control helps you keep and control stock

· Costing helps you calculate the costs for your products or services

· Record-keeping helps you keep and use records

· Financial planning helps you make plans for cash, sales and costs

WHO IS THIS BOOK FOR?

Improve Your Business (IYB) Basics is written for managers of small- and medium- sized businesses. The idea underlying the book is that the most effective improvements come from the active and creative thinking of entrepreneurs themselves and the content therefore is designed to encourage such creative thinking and to motivate entrepreneurs to take action.

The intended reader of IYB Basics is a single manager. This single manager may or may not be the owner of the business, but he or she is the person who makes management decisions.

HOW THIS BOOK WILL HELP YOU

IYB Basics takes a practical approach to business management. Theory is kept to a minimum and the focus is on the day-to-day running of a business. Step-by-step guidelines are often suggested and the reader is encouraged to apply these to his or her own business.

Management methods in six key areas are presented. The Marketing chapter assists you in making strategic decisions in the business, for example, deciding what to sell, to whom and in what way. The Costing and Financial Planning chapters help you to make plans to guide you in running the business and as a help in making management decisions, for example planning cash flow and setting prices. The Buying and Stock Control chapters introduce you to methods for designing and implementing procedures that will help you to run the business more efficiently and more profitably, for example, stock control systems and procedures for buying. The Record-keeping chapter shows you a basic record-keeping system and methods for analysing the records. It helps you to implement control systems to ensure that the business is profitable and to make decisions about the future, for example, to ensure that costs are not rising faster than sales.

In most cases, the best order to read the chapters in IYB Basics is to follow them as they are presented, from Marketing to Financial Planning. For specific purposes, the order can be changed. IYB Basics can be used equally well for self-study and in training, where trainers can benefit from the accompanying IYB Basics Trainer’s Guide.

Since this book is intended for use in many different countries, we have used the term “NU”in the examples to represent an imaginary “National Unit of currency”.

It has been assumed that at the time this material is adapted for any particular country, the country-specific details will also be adapted accordingly.

HOW TO USE IMPROVE YOUR BUSINESS BASICS

In this book you will find:

· Explanations of business management methods. Learn these methods and use them to improve your business.· Practical exercises. Do the exercises in each chapter to practise the business management methods you read about.

· An action plan. Fill in the action plan you will find at the end of the book. This will help you to put your new knowledge into practice.

· Useful business words. Look up the meaning of business words in this section.

· You will also find different types of boxes. Each type of box shows you one kind of information:

|

|

In these boxes, you will find exercises or questions to answer about the content of the chapter. |

|

| |

|

|

In these boxes, you will find answers to the exercises and questions. |

| | |

|

|

These boxes tell you where to find more information in the other chapters. For example: Read more about indirect costs in the COSTING chapter. |

|

| |

|

|

In these boxes, you will find questions about your own business. For example: Do you know your customers’ needs? Does your business provide the right goods or services to satisfy your customers’ needs? |

|

| |

|

|

These boxes tell you something extra important for you to remember. For example: The customer is the most important person for your business. |

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Improve Your Business: Basics (ILO, 1999, 188 p.)

MARKETING

IN THIS CHAPTER YOU WILL LEARN HOW TO

|

NOTE |

Since this book is intended for use in many different countries, we have used the term “NU” in the examples to represent an imaginary “National Unit of currency” |

Understand your customers

WHAT IS MARKETING?

Marketing is everything you do to satisfy the needs of your customers and make a profit by:

· providing the products or services they need

· setting prices that they are willing to pay

· getting your products or services to them

· informing and attracting them to buy your products or services.

|

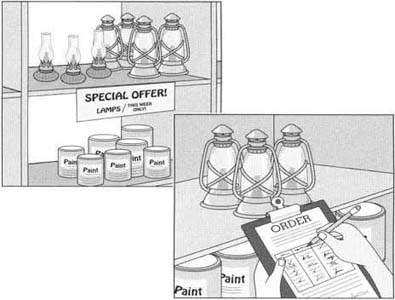

THINK ABOUT WHAT HAPPENS IN THESE BUSINESSES: · A take-away restaurant: A customer asks for a pie but is told that only bread rolls are available. The customer does not buy anything. · A general store: A customer asks for a lamp. He is told that the lamp costs 45 NU but he knows that the same type of lamp costs only 38 NU in another store nearby. The customer does not buy the lamp. 1. The customer does not buy anything to eat from the

take-away restaurant.

Why? 2. The customer does not buy a lamp from the general store.

He buys the lamp from the other store instead.

Why? |

|

1. The customer does not buy anything at the take-away restaurant because it does not have the product the customer wants. 2. The customer buys the lamp from the other store because it is cheaper. |

IS MARKETING IMPORTANT?

Customers are the most important people for your business. If you do not provide what they want, at prices they are willing to pay, and treat them with respect, they will buy somewhere else. Without customers there will be no sales and your business will have to close down.

Satisfied customers will come back and buy more from your business. They will tell their friends and others about your products and your business. More satisfied customers mean larger sales and bigger profits.

Most businesses do not sell as much as they could and many do not understand why. Business people need to know as much as possible about their customers and what they want so they can serve them better. This is the starting point for marketing.

WHO ARE YOUR CUSTOMERS?

Your customers are the people or other businesses who want your products or services and are willing to pay for them.

Your customers are:

· the people who buy from you now

· the people you hope will buy from you in the future

· the people who stopped buying from you but you hope to get back.

Figure

Figure

Here are some examples:

· In most areas, there is a demand for reliable and affordable transport. The customers are all the people who need transport and are willing to pay for it.· In many areas, there is a demand for school uniforms. The school children use the school uniforms but they are not the customers. The parents buy the uniforms for their children. Therefore, the customers for the school uniforms are the parents, or other people who are willing to pay for the uniforms.

· A tailor’s shop makes protective clothing like coats and overalls. They are used by shop assistants, carpenters, and other businesses. The tailor’s shop sells their products directly to other businesses. So, owners and managers of those businesses are their customers.

|

|

Think about the customers of your business. Which are the different kinds of people who want your products or services and are willing to pay for them? |

LEARN ABOUT YOUR CUSTOMERS AND COMPETITORS

Customers buy goods or services to satisfy different kinds of needs and wants. For example, customers buy:

· bicycles because they need transport

· nice clothes because they want to look attractive

· radios because they want information and entertainment

· coats and overalls because they need to protect their clothes.

It is important to know as much as possible about your customers and what they need and want. When you understand your customers’ needs you can decide what products or services to provide. Do market research to understand your customers, make better decisions and increase your sales.

|

|

Your customers are the most important people in your business. Make sure that you sell what your customers want to buy. |

Do market research

To find out about your customers and competitors, ask yourself:

· Which different kinds of customers am I trying to sell to?

· What products or services do they want? Why do they want them?

· What prices are they willing to pay?

· Where are the customers and where do they usually buy?

· When do they buy?

· How often and how much do they buy?

· Who are my competitors, the other businesses selling products and services similar to mine? How good are my competitors?

|

The group of stores in this picture are all of the same type. They sell the same goods to the same customers. Only a few customers buy from each store so sales for each business are low. This happens in many areas. Does it happen in your area?

|

Finding answers to these kinds of questions is called market research. Market research is very important for your business. It means getting information about your customers and competitors.

But it is not enough to know who your customers are and what they want. You must also find out if there are enough customers. Not everybody will buy from your business.

Reliable Tailors used to make school uniforms. The market for school uniforms is large. But by doing market research Reliable Tailors found out that there are too many businesses making school uniforms and that sales for each business are very low.

Reliable Tailors decided to find out about the customers for other products, for example, overalls and protective coats. This is how they found out how many customers there are for protective coats. You can learn about your customers in the same way:

1. Reliable Tailors counted the number of shops in town. There were 80 shops altogether.2. Reliable Tailors asked 10 shops how often they buy new protective coats for their shop assistants. Most said they buy twice every year. Most shops have three people who need protective coats. This means each shop buys six protective coats each year.

3. Some customers will not buy from Reliable Tailors. They will buy from other tailors. Out of the 80 shops in town, Reliable Tailors think they can sell to 40 shops.

4. Reliable Tailors expect to sell 240 protective coats per year.

All businesses need to understand their customers and know about their competitors. Doing market research will help you to satisfy your customers by making decisions on:

· what products or services to sell

· what prices to charge

· how to get your products to your customers

· how to inform customers and attract them to buy.

Market research can be done in many practical ways by you and your employees. Here are some examples of how you can find out more about your customers and competitors:

Talk to your customers or ask them to fill in a questionnaire. Ask them, for example:

· why they buy from you· if they are satisfied with your goods or services and the way they are treated at your business

· if there are other goods or services they would like to buy.

Listen to what your customers say to each other about your business and your goods and services.

Find out why some customers do not stop to buy from your business. Think of yourself. When you want to buy something, why do you go to one business and not to another? Is it because one business has a better product, a better price, better services, or is nearer to you?

Study your competitors’ businesses. Find out about:

· their products or services, for example, quality and design· what prices they charge

· how they attract customers to buy

· what customers say to each other about the goods and services in your competitors’ businesses

· why customers buy from your competitors’ businesses instead of from your business.

Ask suppliers, other businesses and business friends:

· which goods sell well in their businesses

· what they think about your products

· what they think about your competitors’ products.

Check your order books, your sales records and your stock records to find out which goods or services sell well.

Read newspapers, catalogues, trade journals and magazines to get information and ideas on new products or services.

Watch TV and listen to the radio to find out what is popular at the moment and to see what other businesses advertise and how they advertise.

|

|

Have you done market research to find out about your customers and competitors? |

Market research helps a business to know more about their customers and competitors. On the next page you can see how a tailoring business put together the information from their market research.

|

1 |

2 |

3 |

4 |

5 |

6 |

7 |

|

Our products or services |

Our customers |

How often and when do customers buy |

Our price |

Customers’ comments |

Competitor |

Competitor’s price |

|

- protective coats |

- owners and managers of shops, mostly general stores |

- twice every year - mostly in January and June |

- regular price 65 NU |

- good quality - good price- some customers want · more colours |

Qualify Clothing Enterprises - large company - good reputation - good quality - more colours - deliver large quantities - sales people visit customers |

- 70 NU and discounts for large orders |

1. In column 1, write the products or services you sell.2. In column 2, describe the customers for each product or service. Who are the people who want that product or service and are willing to pay for it? For example:

· Are they mostly men, women or children?

· Are they young or old? What type of work do they do?

· Are their incomes low or high?

· Where do they live and where do they buy? In rural areas, in town, near your business or far away?

3. In column 3, write down how often and when your customers buy each product or service. Is it every day, every week, every month, every year, in winter, in summer, on pay day, or after the harvest?4. In column 4, write down what price you charge for each product or service.

5. In column 5, write down what your customers think about your product or your service. For example:

· Do they like the design, the colours, the sizes? Why?

· Do your customers want products or services that you do not have?

6. In column 6, write down other businesses, your competitors, who sell the same or similar products or services as you do. What is special about their businesses, their products or their services?7. In column 7, write down the prices your competitors charge for each product.

|

|

For your market research, it is a good idea to write down information such as: · what customers complain about · ideas for new products or services |

|

Satisfy your customers

You have

· found out about your customers and competitors

· found out if there are enough customers.

Now, use the information about your customers to satisfy their needs. To satisfy the needs of your customers, improve your sales and make a profit, you need to find out:

· what product or service your customers want

· what price your customers are willing to pay

· at what place your business should be so you can reach your customers

· what promotion you can use to inform your customers and attract them to buy your products or services.

These are called the four Ps of marketing. They all start with a P: Product, Price, Place, and Promotion. So they are easy to remember.

|

Right |

+ |

Right |

+ |

Right |

+ |

Right |

= |

MORE CUSTOMERS |

To satisfy your customers and increase your sales, you will need to learn about and use all four Ps of marketing. Satisfied customers will come back to buy more from your business and will tell other people to buy from your business.

All four Ps are very important and must be given strong emphasis. If your business is weak in one or more Ps, you may not be able to satisfy your customers. Your business is in danger and may fail.

Timing of the four Ps is important. The right product, for the right price, at the right place and supported by the right promotion, must be available at the right time. The right time is when the customers require the product.

We will look at each of the Ps one at a time.

1. Product: What products or services to provide

To be successful in business you must have the products or services your customers want. This is called Product and is the first P of marketing.

FIND OUT WHAT CUSTOMERS NEED

Customers buy goods and services to satisfy different needs. For example,

· cold drinks satisfy a need to feel cool in hot weather

· bicycles satisfy a need for transport

· radios satisfy a need for news and entertainment

· clothes satisfy a need to wear something comfortable and a need to feel attractive.

Figure

A successful business finds out what customers want and need. The business provides the products or services to satisfy those needs.

|

|

Do you know your customers’ needs? Does your business provide the right goods or services to satisfy your customers’ needs? |

Sunshine Restaurant is a small restaurant in a good location, where customers can have a quick meal. This is how Sunshine Restaurant satisfies their customers’ needs:

· When they first opened, Sunshine Restaurant only sold cakes and biscuits. But the customers asked for more to choose from, so Sunshine Restaurant started to offer different kinds of food, such as sandwiches and pies.· Later on, customers began to ask for cooked food for lunch. Sunshine Restaurant bought a stove and started serving cooked meals.

· Sunshine Restaurant used to have small paper bags for all take-away foods. Customers started to complain. Now they also use boxes for some soft foods.

Always listen to what your customers like and do not like. When their needs change, change your products and services to satisfy the new needs. Do more market research. When you know what your customers want, you can provide those products or services and increase your sales.

PROVIDE WHAT YOUR CUSTOMERS WANT

Customers want to look at different products so that they can choose what they like best. For example,

· some customers want a different design

· some customers want high quality and are willing to pay extra for it.

If you always provide products or services of the quality your customers want, they will trust you and your business.

|

|

Remember, customers are the most important people for your business. Always keep your eyes open and try to understand their needs, Make sure you provide the products or services the customers want, not what you want. You are not the customer. |

Often ask yourself these kinds of questions:

· What products or services do I sell?

· Why did I decide to sell these products?

· Do I have the products customers want?

· Do I keep products that do not sell well?

If the answers to the questions tell you that customers want different products or services, you can:

· make or sell completely new products, or

· improve what you already make and sell by changing something about your product:

|

the design

|

the comfort

|

the colour

|

|

the size

|

the customer service

|

the guarantee

|

If you sell products which need packaging, you can also change the packaging. Packaging protects your products and makes them easier to handle. Packaging adds to your costs. But packaging can also make your products more attractive and help you increase your sales.

You may decide that products and services other businesses provide are much better than the products or services you can afford to make or sell. The changes you would need to make to your products are too big and would cost too much. When this happens, you decide to stop selling that product. By doing market research, you can decide on a better product or service for your business to sell.

LOOK FOR NEW IDEAS

Your products may not sell very well. Lots of other businesses may sell the same products. Customers may not want your products any more. If the products you sell do not make much profit, think of new ideas. Here are some examples:

If you only make and sell household furniture,

· find new types of customers such as schools and offices by selling school desks, shelves or office furniture.

If you are selling bread,

· find more customers such as restaurants, hospitals and schools.

If you are selling vegetables and fruit,

· think about what new products you can make from vegetables and fruit. You can, for example, make juice and marmalade from oranges.

Before you start making new products, make sure you do market research:

· Think of ideas and ask others. Get as many ideas as possible.· Find out which of those ideas can be made into products that customers would like and would be willing to pay for.

· Make sure there are enough customers who want your new products.

2. Price: What prices to charge

Price is the second P of marketing. Setting prices can be difficult but is very important. Your business may have very good products or services, but if your prices are wrong, you will not sell much.

When you work out a price on a product or a service, you need to know how cost, price and profit work together:

|

Cost |

+ |

Profit |

= |

PRICE |

OR |

Price |

- |

Cost |

= |

PROFIT |

Your total profit from sales depends on:

· how much profit you make on each product or service

· how many of each product or service you sell.

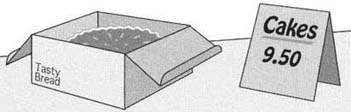

Tasty Bread is a bakery. One of the products they make are cakes which customers buy at the bakery. Tasty Bread have tried both low and high prices:

|

|

|

|

When they put a high price on these cakes, they make a big profit on each cake. But at that price, they only sell one or two cakes a day. |

When they put a low price on these cakes, they make a small profit on each cake. But at that price, they sell many cakes a day. |

| | |

|

Number of products sold x profit per product = total profit | |

|

|

|

|

1 cake x 5 NU profit per cake = 5 NU |

5 cakes x 2 NU profit per cake = 10 NU |

So, you can make a large total profit on a low price. It all depends on how many items of a product you sell and how much profit you make on each item.

HOW TO SET YOUR PRICES

In general, your prices must be:

· low enough to attract customers to buy, and

· high enough to give your business a profit.

You must have certain information before you decide what prices to charge your customers. To set your prices you need to:

· know your costs

· know how much customers are willing to pay

· know your competitors’ prices

· know how to make your prices more attractive.

Know your costs

You must know the total costs of making and selling each product or service. The total costs include materials, labour, rent, electricity, transport and all other costs in your business. To make a profit, your price must be higher than your total costs for the product.

Look at how Sunshine Restaurant set prices. First they must know their costs. The total costs of making one pie are 2 NU. To make a profit, they must sell each pie for more than 2 NU.

|

|

|

| ||||||||||||

| | |

| ||||||||||||

|

LOSS |

NO PROFIT |

PROFIT | ||||||||||||

|

Price |

- |

Cost |

= |

Profit |

Price |

- |

Cost |

= |

Profit |

Price |

- |

Cost |

= |

Profit |

|

1 NU | |

2 NU | |

-1 NU |

2 NU | |

2 NU | |

0 NU |

3 NU | |

2 NU | |

1 NU |

| | | | ||||||||||||

|

-1 NU means a 1 NU loss |

0 NU means no profit |

1 NU means a 1 NU profit | ||||||||||||

| | | | ||||||||||||

|

A price lower than the total cost gives you a loss. |

A price at the same level as the total cost gives you no profit. |

A price higher than the total cost gives you a profit. | ||||||||||||

|

|

The COSTING chapter tells you how to calculate the costs of a product or a service. |

Know how much customers are willing to pay

Customers must be willing to pay your prices. If you set a price which is too high, you will soon know because you will sell very little or nothing.

Sunshine Restaurant asked many customers how much they were willing to pay for a pie. Almost all of them said that 3.50 NU is too much money to pay for a pie. Many of them said they would buy a pie if it does not cost more than 3.25 NU. Sunshine Restaurant now knows that the price for pies should be somewhere between 2.00 NU and 3.25 NU:

· 2.00 NU is the total cost for a pie

· 3.25 NU is the highest price the customers are willing to pay.

If the price customers are willing to pay is lower than your costs, try to cut your costs. If you cannot cut your costs, maybe you need to find another product or service to sell.

Know your competitors’ prices

Find out how much your competitors charge for products or services which are the same or similar to yours.

In general,

· if your prices are lower than your competitors’, you may attract more customers to buy from your business· if your prices are higher than your competitors’, your customers may buy from your competitors.

There may be a reason why you want to charge a higher or lower price than other businesses.

You may want to charge a lower price, for example:

· if your product or service is new and people do not yet know about it

· if you want to attract new customers.

You may want to charge a higher price, for example:

· if customers feel that your product or service is better than the competitors’

· if you provide some extra service such as longer opening hours, free delivery or a good guarantee.

|

|

Be careful: if you try to sell more by cutting prices too much, it can be dangerous for your business. To make a profit, your prices must always be higher than your costs, Therefore it is important to know your costs. |

Sunshine Restaurant found out that most competitors charge 3.25 NU for pies. They now have a lot of information about prices for pies:

· the cost for a pie......................................... 2.00 NU

· the price customers are willing to pay........ 3.25 NU

· competitors’ prices for pies........................ 3.25 NU

Sunshine Restaurant has not yet decided what price to charge for pies. They are thinking of charging 3.00 NU. If customers buy from other places, they have to pay 3.25 NU.

Know how to make your prices more attractive

There are many ways to make your prices sound more attractive to your customers. Sunshine Restaurant decided on a price of 2.99 NU for the pies. 2.99 NU sounds much less than 3.00 NU, even though there is only one cent difference.

To attract customers to come to your business, you can sometimes use special offers - even with low profits. When your customers come for the special offers, they often buy other products as well.

A discount also means a lower price. You can get a discount from a supplier. You can give a discount to a customer. Here are some examples:

|

If a customer buys a large quantity, you can offer a quantity discount. |

If a customer pays cash, you can offer a cash discount. |

At certain times of the year, you can offer a seasonal discount. |

|

| | |

|

|

|

|

|

|

What do you do to make prices in your business more attractive? |

3. Place: How to reach your customers

Your business may have good products at prices that customers are willing to pay, but sales may still be low. The reason may be that customers do not know where to buy your products or services.

The third P in marketing is called Place. Place means location - where your business is. Location is especially important for retailers and service operators, who need to be where it is convenient for their customers.-

Place also means different ways of getting your products or services to your customers. This is called distribution. Distribution is especially important for manufacturers.

LOCATION - WHERE YOUR BUSINESS IS

Before Sunshine Restaurant was started the owner thought about where to locate the business. She wanted to know which place would be best for her customers.

|

In the residential area? |

In the business centre? |

Where the small manufacturers are? |

|

|

|

|

|

· To sell well, most retailers and service operators need to be where their customers are. Good places for retailers and service operators are where many people pass by or where many people live. · For example, a good place for a take-away restaurant is near a bus station at a business centre. A lot of people pass there. An area where many small manufacturers work is also a good place for a take-away restaurant. Workers want to buy something to eat for lunch. · A residential area is not a good place because most people are away during the day or they cook their own food in their homes. 1. Where is a good place for a grocery store?

Why? 2. Where is a good place for a taxi business?

Why? |

|

1. A good place for a grocery store is near where customers live. Customers can then easily get to the store and carry their groceries home. 2. A good place for a taxi business is where there are lots of people who often need to; travel. For example: · where people look for transport to go to work or to come home from work · at shops and hotels. |

|

|

Why have you located your business where it is? Is it a good place? Why? Is there a better place for your business? |

|

|

Make sure your business is not in a place where there are too many other businesses selling the same products or services you sell. |

DISTRIBUTION - GETTING YOUR PRODUCTS TO YOUR CUSTOMERS

For manufacturers it is not always important to be near their customers. It is often more important to have:

· a cheap rent

· a reliable and convenient supply of raw materials.

If your business is not where your customers are, you must find ways to get your products to where it is easy for customers to buy. This is called distribution. Distribution is particularly important for manufacturers.

There are different ways to distribute your products to your customers:

· You can sell directly to the customers who use your products. This is called direct distribution.· You can sell to other businesses which then sell your goods to consumers or other businesses. Those businesses are mostly retailers or wholesalers. This is called retail distribution and wholesale distribution.

Direct distribution

Direct distribution means selling your products directly to the customers who use them.

When you sell your products directly to the customers who use them, you can talk to them and find out what they like, want and can afford. So, direct distribution is most useful for those manufacturers who make products to each customer’s order.

|

DIRECT DISTRIBUTION | ||

| | | |

|

Manufacturer |

® |

Customer |

| |

| |

|

makes the product |

|

uses the product |

Direct distribution is useful for some businesses. But it takes time and it can be expensive for your business. For example, think of the costs for transport, wages or your salary, for the time you or your employees spend selling or delivering goods to customers.

|

DIRECT DISTRIBUTION is most useful for your business if you: · make specialized products, where you need to discuss the product with the customer - for example, making clothes or furniture to each customer’s order · have few customers so you can keep in contact with each of them - for example, making carriers for a large bicycle manufacturer · make fairly expensive products that customers do not buy very often - for example, making carts · provide a service with the product you make - for example, making burglar bars and putting them up for the customer. |

Retail distribution

Retail distribution means selling your products to shops and stores who then sell to the customers who use the products.

Retail distribution is useful for businesses that make products in large quantities. Retailers often reach more customers in a larger area than your business can do on its own. So, when you sell your products to retailers you reach more customers, your sales may increase and your business can grow.

|

RETAIL DISTRIBUTION | ||||

| | | | | |

|

Manufacturer |

® |

Retailer |

® |

Customer |

| |

| | |

|

|

makes the product |

|

buys and sells the product | |

uses the product |

Retailers can do a lot of work that your business has to do on its own if you sell directly to the customers who use your products. For example, retailers:

· keep in contact with customers. This gives you more time for production and other important activities.· stock your products. This helps your business to have less money tied up in stock.

· help promote your products by advertising, etc.

Retailers do a lot of work that your business would have to pay for otherwise. Because of that you charge them a lower price than you would charge the customers who use your products. On the other hand, retailers often pay you immediately when they get your products.

|

RETAIL DISTRIBUTION is most useful for your business if you make goods in large quantities, and you: · make standard products which normally do not need a lot of contact with customers about design, colour, size, etc. - for example, making hair oil or shampoo · make low-priced products that customers buy often - for example, making soap · have many customers and it takes a lot of time to stay in contact with each customer - for example, making standard cups and plates · have customers in a large area so that it is difficult, takes time, and is expensive to reach all of them - for example, making farming equipment. |

Wholesale distribution

Wholesale distribution means selling your products in very large quantities to wholesalers who sell them in smaller quantities to retailers.

Wholesale distribution is useful for businesses that make products in very large quantities. Wholesalers can normally reach even more customers in a larger area than retailers can. So, when you sell your products to wholesalers, you reach even more customers, your sales may increase and your business can grow.

Wholesalers sell to retailers who then sell to the customers who use your products. Like retailers, wholesalers do a lot of work that your business otherwise would have to do on its own. For example, wholesalers:

· keep in contact with retailers who buy your products

· stock and transport your products

· promote your products.

|

WHOLESALE DISTRIBUTION | ||||||

| | | | | | | |

|

Manufacturer |

® |

Wholesaler |

® |

Retailer |

® |

Customer |

| |

| | |

| | |

|

makes the product |

|

buys from manufacturer and sells to retailer | |

buys from wholesaler and sells to customer | |

uses the product |

Wholesalers do a lot of work that your business would have to pay for otherwise and can help you to reach many more customers in a very large area. Because of that you normally charge them an even lower price than you would charge a retailer.

|

WHOLESALE DISTRIBUTION is most useful for your business if you: · make low-priced, standard

products in very large quantities, and |

Which type of distribution is best for your business?

Each type of distribution is useful for different types of businesses. Before you decide if you want to change your distribution, think about:

Your products

· Do you make standard products or products to each customer’s order?

· Do you make low-priced products or high-priced products?

· Do you provide any special service with your products?

Your customers

· Do you have many or few customers?

· Where are your customers? Nearby or far away?

· How much do they usually buy?

Your business

· What does your business have difficulties with? Would your business improve if someone else does the selling, stocking, promoting, etc.?· What can your business do best on its own? If you sell to retailers or wholesalers, will your business improve? How?

Your sales, costs and profit

· How much can you sell with each type of distribution?· Can you make and sell enough to supply retailers or wholesalers with the quantities they want?

· Which type of distribution will give your business the highest sales and the highest profit?

4. Promotion: How to attract customers to buy

Your business may be in a good place, have good products at prices that customers are willing to pay, but your sales may still be low. Why?

Maybe it is because you do not tell people about your business and what it can offer. This is called Promotion and is the fourth P of marketing. Promotion means informing and attracting people to buy your products or services.

Decide how much you can spend on promotion and what types of promotion to use. Promotion sometimes costs a lot and it is important to use the best type of promotion for your business.

Do not sit and wait for customers to come to you. Do promotion, sell more and increase your profit by:

· advertising - making customers interested

· sales promotion - getting customers to buy more

· publicity - getting free promotion

· improving your skills as a salesperson.

ADVERTISING

Advertising is giving information to people to make them more interested in buying your goods or services. Let us look at some ways to do good advertising for your business.

Signs

Use signs so that people know and remember the name of your business, what it sells, where it is, when it is open, and so on. Bright colours, clear writing and a picture or symbol will make more people see your signs. Do not put too much information on your signs. It is difficult to read a sign with a lot of information. It is a good idea to find a good, local sign-painter to help you.

Boards, posters and leaflets

Use boards, posters and leaflets to tell customers about special offers, discounts, new products, and so on. You can use paper or chalk and a chalkboard.

Write on the boards, posters and leaflets. Make your posters big enough so that people will notice them. Use the information from your market research and put the posters where many people can see them. Give leaflets to people who may be interested in buying your products or services.

Business cards, price lists, special letters and photos

Use business cards to tell people who you are, the name of your business, your location and what you sell. Use a price list to tell people about all the products you sell and how much they cost. Write special letters to promote your business to people you think will be interested in buying your products or services.

You can use a rubber stamp to make your own business cards and letterheads. To give a good impression make sure that your letters are neat and that the information is clear. Ask customers to give your price lists and business cards to their friends and other people who may be interested in your products or services.

Newspapers, radio and television

· Advertising in the local newspaper is sometimes good but it is usually quite expensive.· Advertising on the radio can be useful in some places - especially if there are many people who do not read and write but often listen to the radio.

· Advertising on television is expensive and is often used by large businesses who want to reach many customers in a large area.

Figure

When you advertise, think about what customers would like to know. Customers want to know:

· what products or services you sell

· your prices and terms

· where they can buy your products

· why they should buy from your business. What is special or different about your business, your products or services.

SALES PROMOTION

Sales promotion is everything you do to make customers buy more when they have come to your business. You can do sales promotion in many different ways.

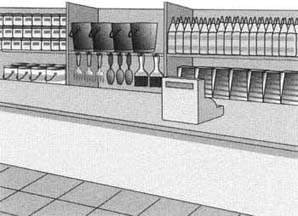

Displays

Display is the way you arrange your products. Display is important for all businesses, especially for shops and stores. Good display makes it easier for customers to see your products so they can choose and buy.

Keep your business:

· well organized

· well lit, clean and fresh-looking

· attractive, with your products well displayed.

On the opposite page are some ideas on how to display your goods to increase your sales:

|

1. Put your goods in groups Put similar products next to each other. This makes it easier and quicker for customers to find what they are looking for. For example: · put hot drinks like tea, coffee and cocoa together · put all cleaning materials together |

2. Make your shelves look full Do not keep a lot of goods in your storeroom. Keep most of your goods where customers can see them and buy them. Do not let your shelves get empty before you fill them again. Empty shelves make your business look badly stocked. Move goods towards the front of the shelves to make the shelves look full. |

3. Show the front of the packages The front of a package usually looks bright and attractive. This makes it easier for customers to see their favourite products and to be attracted to new products. |

|

| ||

|

4. Put goods where they can be seen easily If your business has a counter, do not have too much space between the shelves and the counter. If customers can see your products clearly, they may decide to buy. Put small items such as sweets in glass shelves, or buttons in glass jars, so customers can see them. |

5. Put goods at the customer’s eye level Customers will see and buy goods which are at the same level as their eyes. It is more difficult to see goods near the floor or high up on a shelf. If you need to use those shelves, only use them for well-known products which customers often buy. |

6. Show the prices clearly Customers want to know the prices of your goods without having to ask you. You can show the price on the edge of the shelf, below each different product. Write large enough for the customers to see the price clearly. |

More ideas for sales promotion

Let customers try new products

Let customers try or taste new products, to interest them in buying the new products.

Make special offers

Use special offers to sell more of your regular goods, seasonal goods or new goods. You can also use special offers for goods which have been selling slowly and goods which are slightly old or damaged.

Give demonstrations

Show customers how to use products that are technical or difficult to understand. When customers can see how something works and how well it works, they become more interested in buying.

Sell products that go together

To sell more, put products that go together next to each other. Torches and batteries go together. They are not useful on their own. Remind customers to buy them.

There are no rules for sales promotion, but remember:

· Be creative, use your own ideas and try something different.· Keep customers interested. Change the type of sales promotion often and only use each for a short time.

· Do not use too many types of sales promotion at the same time. Customers may feel you are forcing them to buy.

Figure

PUBLICITY

Honey Bee is a successful bee-keeping business. A journalist wrote a story about the business in the local newspaper. Because of the story many people found out about their products and sales increased for Honey Bee. They got publicity.

Publicity is free promotion through an article in a newspaper or magazine which tells people about your products or services. The article promotes your business. Good publicity increases your sales.

Publicity works well because:

· people who do not read advertisements may read the article about your business

· people believe what they read in an article more than they believe advertisements.

It is not easy to get publicity for your business. You can write an interesting letter to a local newspaper, magazine or the radio and describe what your business does and how it serves the community. If they think they can make a good article about your business they might come and interview you.

Word of mouth - what people say about your business

There is another type of publicity which is free. It is probably the most common way new customers find out about your business. It is called word of mouth. Word of mouth means that people tell others what they think about you, your business and what you sell. The word travels from one person to another. Make sure it is a good word so it gives your business a good reputation.

Word of mouth can also be bad for your business. Bad words about your business travel very fast - almost like a fire. It takes a long time to build a good reputation again. So, always make sure that customers talk well about you, your employees and the products or services your business sells.

IMPROVING YOUR SKILLS AS A SALESPERSON

You have attracted customers to come to your business with good advertising and good sales promotion. But your product or service is not yet sold. How well you will sell now depends on you. Your skills as a salesperson can make the difference between success and failure.

How to be a successful salesperson

To improve your skills as a salesperson and increase your sales you need to:

· know your customers and their needs

· know how to treat your customers

· know your products and how to sell them.

Know your customers and their needs

Customers are different. For example:

· some customers can never make up their minds

· some customers are always in a hurry

· some customers never have enough money.

To be successful, try to understand and get to know every customer. First find out what the customer really needs by listening and asking questions. Then satisfy the customer’s needs by:

· giving advice

· offering suitable products or services.

Know how to treat your customers

Successful salespeople try to see things through the customer’s eyes. This means that you should try to think of yourself as a customer.

Treat your customers the way you like to be treated when you are a customer:

· Greet your customers. Call them by their names.· If you are already serving a customer, greet new customers and tell them that you will soon help them.

· Be polite and friendly so that customers feel welcome and enjoy visiting your business.

· Do not talk too much. Listen carefully to what your customers say and ask questions to find out what they need.

· Be patient. Give the customers time to ask questions and decide if they want to buy.

· Always be honest and trustworthy. For example, tell your customers the good and bad points about a product or a service.

· Do not disagree with your customers if they decide they do not want a product. Allow them to say no.

· Never argue with a customer. Make your customers feel they are right.

· Thank your customers for coming to your business.

|

|

Customers are the most important people for your business. Treat customers the way you like to be treated when you are a customer. |

Know your products and how to sell them

To get respect and trust from your customers and to sell well, you need to know your products. Your customers may ask many questions about your products, or services. Be sure you know the answers.

|

|

|

|

|

· Do I use it with cold water or

hot water? |

· How do I keep it clean and

shiny? |

· Is the material

strong? |

Even if you know your products very well, you may still not sell much. The reason can be that you do not know how to show and explain your products to your customers. For example, if you are selling a radio and tell the customer that the radio has short and medium wave bands, earphones and a manufacturer’s guarantee, the customer might not understand these technical details.

To make it easier for customers, a skilled salesperson:

· first tells the customer what the product can do and how it can be useful

· then gives the technical information that is needed.

If you are selling a radio you can explain the details this way:

· “You can listen to all local programmes very clearly. You can also listen to many programmes in other countries because this radio has both short and medium wave bands.”· “You can listen without disturbing others because this radio has earphones. When you use the earphones, only you can hear.”

· “If you have any problems with this radio in the first six months, we will repair it free of charge because the manufacturer gives a six-month guarantee.”

|

|

What type of salesperson are you? What do you think your customers say about you as a salesperson? |

Review

Summary

Marketing is everything you do to satisfy the needs of your customers and make a profit by:

· providing the products or services they need

· setting prices that they are willing to pay

· getting your products or services to them

· informing and attracting them to buy your products or services.

Your customers are the people or other businesses, who want your products or services and are willing to pay for them.

Do market research to learn about your customers and competitors.

The first P of marketing is Product. Product means having the products or services your customers want.

Customers buy goods and services to satisfy different needs and wants. A successful business finds out what customers need and then provides the products or services to satisfy those needs.

Keep your eyes and ears open for ideas about new products or services.

The second P of marketing is Price. In marketing, price means:

· setting a price that your customers are willing to pay

· making sure the price is attractive and still gives you a high enough profit.

Before you set a price, you need to know:

· your costs

· how much customers are willing to pay

· your competitors’ prices

· how to make your prices more attractive to your customers, for example by using special offers and discounts.

The third P of marketing is Place. Place means:

· location - where your business is located, and

· distribution - how to get your products or services to your customers.

Most retailers and service operators need to be where it is convenient for their customers. Manufacturers need to have a good way of distributing their products to their customers.

Direct distribution is most useful for your business if you make fairly expensive, specialized products and have few customers who may want a service with the product you make.

Retail distribution and wholesale distribution are most useful if you make a large quantity of standard, low-priced goods and have many customers in a large area.

The fourth P of marketing is Promotion. Promotion means informing and attracting the customers to buy your products or services.

Do promotion, sell more and increase your profit by:

· advertising

· sales promotion

· publicity

· improving your skills as a salesperson.

Use advertising to make customers more interested in buying your products or services.

Use sales promotion to make customers buy more when they have come to your business.

Publicity is free promotion. For example, a good story about your business in a newspaper or on a radio gives you good publicity. Word of mouth means that people tell others what they think about you, your business and what you sell.

Improve your skills as a salesperson. To be a successful salesperson and increase your sales you need to:

· know your customers and their needs

· know how to treat your customers

· know your products and how to sell them.

What did you learn in this chapter?

Now that you have worked through this chapter, try these practical exercises. The exercises will remind you of what you have learned and help you to improve the marketing in your business.

Compare your answers with the Answers. If you find it difficult to work out an answer, read the relevant part of the manual again. The best way to learn is to finish an exercise before you look at the answers. Check the list of Useful Business Words.

|

|

You have learned more about marketing in this chapter. But what you have learned does not help until you use the new knowledge in the day-to-day running of your business. Remember to do the Action Plan to improve the marketing in your business. |

Marketing at Beauty Hair Salon

Beauty Hair Salon is located in the middle of the business centre in a small town. Beauty Hair Salon have friendly, qualified employees and a good reputation. Customers come to Beauty Hair Salon for trimming, styling, washing, cutting and colouring.

Beauty Hair Salon have noticed that some women in the business centre have a perm which is a new fashionable hairstyle. They do not do perms. Beauty Hair Salon want to increase their sales. So they do market research to find out about offering a new product, perms.

The following is the information Beauty Hair Salon found about perms in their market research.

|

1 |

2 |

3 |

4 |

5 |

6 |

7 |

|

Our products or services |

Our customers |

How often and when do customers buy |

Our price |

Customers’ comments |

Competitors |

Competitors’ price |

|

- Perms |

- young women who shop or work in the business centre - women with high status jobs, e.g. business women, secretaries, office clerks, teachers - women with fairly high income - a bank and a large commercial office will soon be opening in the business centre - 30 customers who came to Beauty Hair Salon last week said they wanted and could afford perms |

- every three months · a perm lasts for three months - restyle once a month · a perm can be changed into different styles |

- to be decided - the cost of a perm is 70 NU |

Customers want: - to look attractive - to look wealthy enough to afford a fashionable hairdo - the most fashionable hairstyle - low prices - hairdos that last a long time - perms that can be changed into different styles |

Fashionable Hair Care offer perms. They have: - a very good reputation - high prices but offer discounts - very qualified employees - knowledge about the latest hairstyles - 0.5 km from the business centre Top Hairstyles offer perms. They have: - a poor reputation - quite high prices - unqualified employees - 2 km from the business centre |

Fashionable Hair Care: Top Hairstyles: |

|

MARKETING AT BEAUTY HAIR SALON What advice can you give Beauty Hair Salon about the new products? Think about the 4 Ps of marketing: Product, Price, Place and Promotion. Use the information from Beauty Hair Salon’s market research to answer these questions: 1. Product: What needs do customers have that Beauty

Hair Salon do not

satisfy? 2. Price: Can you advise Beauty Hair Salon what price

to charge for a perm? Explain how you set the

price. 3. Place: Is Beauty Hair Salon in a good place? Why or

why

not? 4. Promotion: If Beauty Hair Salon decide to offer

perms, what types of promotion do you suggest they can use to attract customers?

Think of as many ideas as

possible. 5. Is it a good idea for Beauty Hair Salon to offer perms?

Why or why

not? |

|

Answers to MARKETING AT BEAUTY HAIR SALON 1. Customers have the following needs that Beauty Hair Salon do not satisfy: · The need to look fashionable - Beauty Hair Salon do not offer fashionable hairstyles such as perms. ____________________________________________________________________ 2. First, to set their price Beauty Hair Salon must know the costs. The costs of a perm are 70 NU. So, to make a profit, Beauty Hair Salon must charge a price which is higher than 70 NU. Then, Beauty Hair Salon need to think about competitors’ prices and what price customers are willing to pay: · Top Hairstyles charge TOO NU. They have a poor reputation, unqualified employees and are 2 km from the business centre. Beauty Hair Salon have a good reputation, qualified employees and they are near their customers. So, Beauty Hair Salon should charge a price which is higher than 70 NU - the cost of a perm. The best price for Beauty Hair Salon to charge is probably: · higher than 100 NU - the price at Top Hairstyles Beauty Hair Salon can also think of ways to make the price for perms more attractive. For example, they can offer a special introductory price or give some other types of discount. ____________________________________________________________________ 3. Yes, Beauty Hair Salon is in a good place. Their location in the middle of the business centre is convenient for their customers. Fashionable women with fairly high incomes work in the business centre and many other women come to the business centre for shopping, or to find transport. When the bank and the large commercial offices open, there will be even more customers. Then Beauty Hair Salon’s location will be even better. ____________________________________________________________________ 4. Beauty Hair Salon can use many types of promotion. They can: · Put a sign in their window, or a board outside the salon, saying that they do the latest, fashionable perms. ____________________________________________________________________ 5. Yes, it is most likely a good idea for Beauty Hair Salon to offer perms because: · The product will satisfy their customers’ needs to look attractive, fashionable and wealthy. · They can make a profit on perms. Beauty Hair Salon can charge between 100 NU and 120 NU, which is more than the cost of 70 NU. |

|

|

| ||||||||||||||||||||||||||||||||||||||||||||||||

Improve Your Business: Basics (ILO, 1999, 188 p.)

BUYING

IN THIS CHAPTER YOU WILL LEARN HOW TO

|

NOTE |

Since this book is intended for use in many different countries, we have used the term “NU” in the examples to represent an imaginary “National Unit of currency” |

Buying to sell

WHAT IS BUYING?

Businesses buy raw materials, goods and equipment to:

· make products to sell

· provide services

· resell.

Here are some examples:

|

|

® |

|

|

A metal workshop buys equipment and raw materials such as metal sheets, nuts, bolts, welding equipment and tools. | |

It uses the equipment and the raw materials to make and sell products such as gutters, buckets and feeders. |

| | | |

|

|

® |

|

|

A hardware store buys goods such as paints, fertilizer and tools. | |

It resells the goods to customers. |

IS BUYING IMPORTANT?

|

THINK ABOUT WHAT HAPPENS IN THESE THREE BUSINESSES: · A tailoring business Quality Tailors are convinced by a supplier’s sales representative that a new thin silky material is very popular and that the customers will like it. The material is expensive but they buy 50 metres. Unfortunately the demand for the material is low and one year later Quality Tailors still have 40 metres in stock. · A bakery Village Bakery run out of flour very often. Sometimes they have to go to town to buy flour three times a week. · A general store Star Store buy a lot of soap powder but do not manage to sell any of it because their customers want bars of soap. 1. What is the problem with the way Quality Tailors do their

buying? 2. What do Village Bakery do wrong in their

buying? 3. What do Star Store do wrong in their

buying? |

|

1. The problem with Quality Tailors’ buying is that they do not know what their customers want. They buy what the supplier tells them to buy. 2. Village Bakery do not buy enough flour and often run out. It takes a lot of time and costs a lot of money for transport for them to go to town to buy more. 3. Star Store bought too much soap powder. Their customers do not want soap powder. They want bars of soap. |

|

|

Buy the goods, material or equipment that give your business the best profit. Before you buy, make sure you know what your customers want. Read about how to do market research in the MARKETING chapter. |

WHAT YOU BUY FOR YOUR BUSINESS

Businesses need to buy:

Equipment

Equipment is all the machinery, tools, workshop fittings, office furniture, etc., that your business needs. Equipment is expected to last for a long time and is often expensive. When you need to buy equipment, find out as much as you can about all the different types of equipment you could use. Your equipment will need repairs. Ask the supplier about spare parts and repairs before you buy any equipment.

Raw materials

Manufacturers need raw materials to make goods to sell. Raw materials are all the materials and parts that go into the products you make. Before you buy raw materials, find out what different materials you need and what quality of raw materials you need.

Finished goods

Wholesalers and retailers buy and sell finished goods made by manufacturers. Do market research and think carefully before you buy finished goods. Buy goods that your customers want.

BUY WELL TO IMPROVE YOUR BUSINESS

When you buy equipment, raw materials or finished goods:

Buy the right quality

Buy the quality of goods your customers want.Buy the right quantity

Buy the quantities your business needs and your customers want - not too much or too little.Buy at the right price

Buy at prices your business can afford and your customers are willing to pay. Make sure that the prices you pay give your business the profit it needs.Buy at the right time

Buy when your customers and your business need the goods, materials or equipment - not too early or too late.

|

|

The MARKETING chapter tells you more about how to decide which finished goods to buy and sell. The STOCK CONTROL chapter tells you more about buying the right quantities of goods and materials at the right time. |

Steps to follow when you buy

There are certain steps to follow when you buy goods, materials, equipment or anything else your business needs. You can follow the same steps for any kind of business.

|

STEP 1. |

Find out what your business needs | | |

| | |

| |

|

STEP 2. |

Get information about different suppliers | |

|

|

| | |

|

|

STEP 3. |

Contact the suppliers |

USE THIS BUSINESS DOCUMENT ® |

ENQUIRY |

| | | | |

|

STEP 4. |

Choose the best suppliers for your business |

USE THIS BUSINESS DOCUMENT ® |

QUOTATION |

| |

| | |

|

STEP 5. |

Make the order |

USE THIS BUSINESS DOCUMENT ® |

ORDER |

| | | | |

|

STEP 6. |

Check the goods immediately |

USE THIS BUSINESS DOCUMENT ® |

DELIVERY |

| |

| | |

|

STEP 7. |

Check the invoice |

USE THIS BUSINESS DOCUMENT ® |

INVOICE |

| | | | |

|

STEP 8. |

Pay |

USE THIS BUSINESS DOCUMENT ® |

RECEIPT |

All eight steps are important. When you choose new suppliers, it is especially important to follow steps 1, 2, 3 and 4.

STEP 1. FIND OUT WHAT YOUR BUSINESS NEEDS

Make sure you know as much as possible about your customers - who they are and what they need and want. Here are some important questions to ask yourself before you decide what your business needs:

- Which different kinds of customers am I trying to sell to?

- What products or services do they want? Why do they want them?

- What prices are they willing to pay?

- How often and how much do they buy?

- Where and when do they usually buy?

- Who are my competitors and how good are they?

When you know what your market wants, you as a buyer can make better decisions about:

· what materials or equipment you need if you make goods to sell

· what goods you need if you resell finished goods

· what quantities you need

· what prices you are prepared to pay

· when you need the goods or materials.

|

|

The MARKETING chapter tells you more about how to understand and satisfy the needs of your customers with the goods or services they want. |

STEP 2. GET INFORMATION ABOUT DIFFERENT SUPPLIERS

Find out which suppliers sell the goods, materials or equipment you need. There are many ways to find out:

· Ask the people who work with you, your business friends, your business trainer, or others. Also, find out from your competitors where they buy.· Contact organizations that support small businesses, for example, the local Chamber of Commerce. They sometimes know about useful, reliable suppliers.

· Look in newspapers, magazines and trade journals. Sometimes there is a list of businesses at the back of the telephone book.

For each supplier, find out as much as possible about what goods, materials or equipment they offer, prices and discounts, credit, deliveries and so on. Try to find out from others how reliable each supplier is. For example:

· Does the supplier usually deliver on time?

· Does the supplier accept returned goods or materials?

· How responsible is the supplier for the quality of goods and materials?