World Energy Assessment - Energy and the Challenge of Sustainability (UNDESA - UNDP - WEA - WEC, 2000, 517 p.)

PART II. ENERGY RESOURCES AND TECHNOLOGY OPTIONS

Chapter 5. Energy Resources

(introduction...)

Definitions and units

Oil reserves and resources

(introduction...)

Ultimately recoverable resources - the static or geologists’ view

Available resources - the dynamic or economists’ view

Reconciling the two views

Gas reserves and resources

(introduction...)

Conventional gas

Unconventional gas

Coal reserves and resources

(introduction...)

Current resources and reserves

Additional resources

Summary of fossil resources

Reserves and resources of fissile materials

(introduction...)

Uranium reserves

Uranium resources

Thorium reserves and resources

Hydroelectric resources

(introduction...)

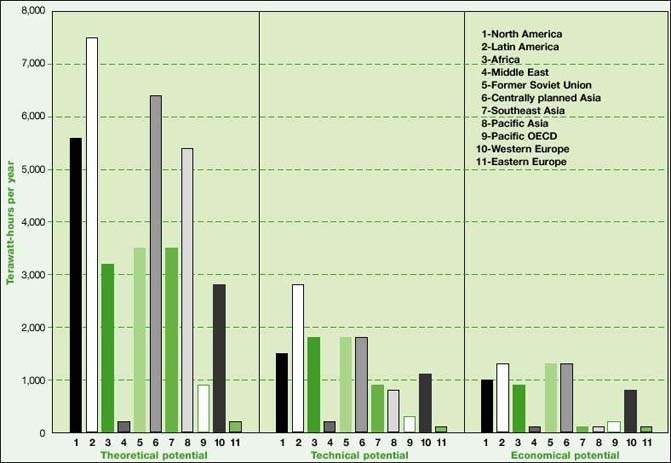

Theoretical potential

Technical potential

Economic potential

Major constraints to hydroelectricity expansion

Biomass resources

(introduction...)

Sources

Perceptions and problems

Technical potential of biomass energy plantations

Energy balances and biomass productivity

Agricultural and forestry residues and municipal waste

Environmental implications of biomass production

Environmentally motivated responses to biomass production

Economics

Solar energy resources

Wind energy resources

Geothermal energy resources

Ocean energy resources

Conclusion

Chapter 6. Energy End-Use Efficiency

(introduction...)

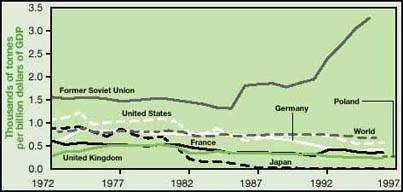

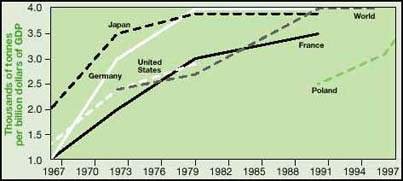

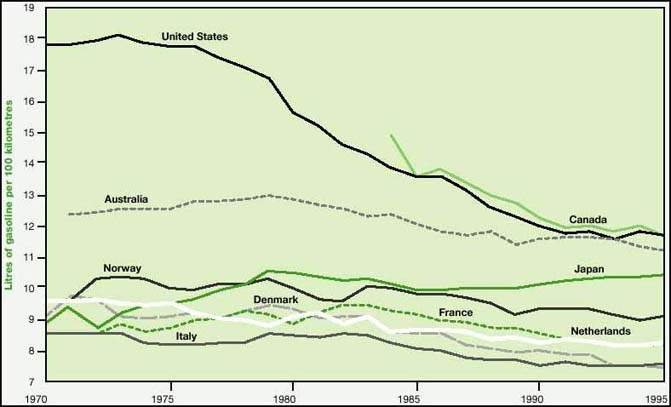

Recent trends in energy intensity in countries and regions

(introduction...)

OECD countries

Eastern Europe and the Commonwealth of Independent States

Developing Asia, Africa, and Latin America

Potential benefits of technology transfer

(introduction...)

Transition economies

Developing countries

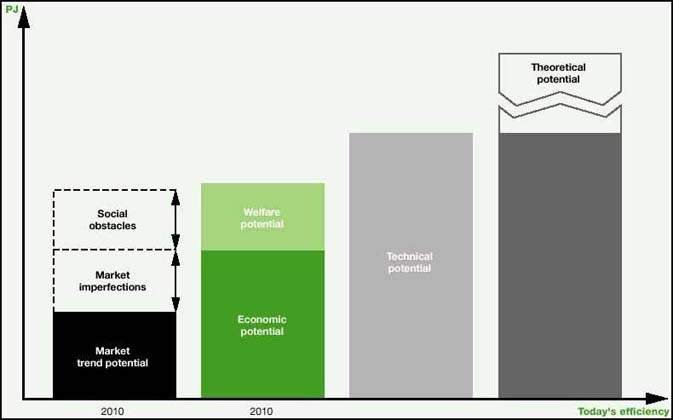

Types of potential for increased energy efficiency

The economic potential of energy efficiency by region and sector

(introduction...)

Western Europe

North America

Japan and Southeast Asia

Eastern Europe

Russia and other members of the Commonwealth of Independent States

India

China

Latin America

Africa

The economic potential of energy efficiency - a systemic perspective

Technical and theoretical potentials for rational energy use after 2020

Obstacles, market imperfections, and disincentives for efficient energy use

(introduction...)

General obstacles

Target group-specific and technology-specific obstacles

National and international policies to exploit the economic potential of energy efficiency in end-use sectors

(introduction...)

General policy measures

Sector- and technology-specific policy measures

International policy measures

Conclusion

Chapter 7. Renewable Energy Technologies

(introduction...)

Biomass energy

(introduction...)

The potential of biomass energy

Biomass energy conversion technologies

Environmental impacts of biomass energy systems

Economics of biomass energy systems

Implementation issues

Conclusion

Wind energy

(introduction...)

The potential of wind energy

Development of installed wind power

Technology developments

System aspects

Environmental aspects

Economic aspects

Implementation issues

Conclusion

Photovoltaic solar energy

(introduction...)

Characteristics of the source

The potential of photovoltaic solar energy

Photovoltaic market developments

Current status and future development of photovoltaic solar cells and modules

System aspects

Environmental aspects

Economic aspects

Implementation issues

Space-based solar energy

Conclusion

Solar thermal electricity

(introduction...)

The potential of solar thermal electricity

Solar thermal electricity market developments

Solar thermal electricity technologies

Economic aspects

Environmental and social aspects

Conclusion

Low-temperature solar energy

(introduction...)

Low-temperature solar energy potential and market developments

Low-temperature solar energy technologies and systems

Implementation issues

Conclusion

Hydroelectricity

(introduction...)

The potential of hydroelectricity

Hydroelectric technology development

System aspects

Environmental and social impacts

Economic and financial aspects

Conclusion

Geothermal energy

(introduction...)

The potential of geothermal energy

Recent developments

Potential market developments

Environmental aspects

Conclusion

Marine energy technologies

(introduction...)

The potential and technology of marine energy

Economic aspects

Environmental aspects

Implementation issues

Conclusion

System aspects

(introduction...)

Trends in the energy sector

Characteristics of renewable energy systems

Electrical system design

Grid integration of intermittent renewables

Intermittent renewables and energy storage

Value of renewables

Conclusion

Policies and instruments

(introduction...)

Cost of competing conventional energy

Financing and fiscal policy

Regulation

Getting new technologies started

Conclusion

Chapter 8. Advanced Energy Supply Technologies

(introduction...)

Advanced fossil energy technologies

Fossil fuel supply considerations as a context for fossil energy innovation

Setting goals for advanced fossil energy technologies

Technologies and strategies for moving towards near-zero emissions

Other near-term advanced fossil energy technologies

Conclusion

Advanced nuclear energy technologies

(introduction...)

Rationale for reconsidering the nuclear option

The need for advanced technologies

Advanced nuclear generating options for the immediate future

Nuclear energy for the long term

The outlook for addressing the challenges

World Energy Assessment - Energy and the Challenge of Sustainability (UNDESA - UNDP - WEA - WEC, 2000, 517 p.)

PART II. ENERGY RESOURCES AND TECHNOLOGY OPTIONS

Chapter 5. Energy Resources

Hans-Holger Rogner (Germany)

LEAD AUTHORS: Fritz Barthel (Germany), Maritess Cabrera

(Philippines), Andre Faaij (Netherlands), Marc Giroux (France), David Hall

(United Kingdom), Vladimir Kagramanian (Russian Federation), Serguei Kononov

(Russian Federation), Thierry Lefevre (France), Roberto Moreira (Brazil), R.

N�tstaller (Austria), Peter Odell (United Kingdom), and Martin Taylor (United

States and United Kingdom)

ABSTRACT

A comprehensive account of the world’s energy resource

endowment is essential for any long-term energy assessment. Energy resources

exist in different forms - some exist as stocks and so are exhaustible, others

exist as flows and are inexhaustible, and a third form is based on exhaustible

stocks that can be leveraged to resemble renewables. Most important, energy

resources evolve dynamically as a function of human engineering ingenuity,

driven by the desire to supply affordable and convenient energy services.

Although the term stocks suggests finiteness (which is ultimately correct), the

accessible portion depends on technology and on the future demand for that

resource. Resources not demanded by the market are ‘neutral stuff’.

Demand plus advances in technology and knowledge turn neutral stuff into

reserves that are replenished upon use by further advances in technology and

knowledge, enabling humans to tap into resources previously beyond reach. But

for stocks there will eventually be a limit. In contrast, resources based on

annually recurring flows are distinctly different from stocks: harvested

prudently, they are renewable. But resources are not an end in themselves, and

their attractiveness must be seen in the context of societies’ energy

service needs, of the technologies that convert resources into energy services,

and of the economics associated with their use. This chapter assesses whether

long-term energy resource availability could impede sustainable development and,

based on a dynamic technology concept, provides a comprehensive account of the

world’s energy resource endowment.

This chapter reviews fossil,nuclear, and renewable

energy resources. The reserve and resource volumes presented here cover the

ranges considered robust by most of the lead authors. The main controversy yet

to be resolved concerns the different views on the roles of technology and

demand in the long-term availability of a particular resource. Subject to debate

is the extent to which reserves can be converted from additional conventional

resources with lower geological assurance and from unconventional resources

lacking economic attractiveness given current markets and technologies. Natural

flows are immense for renewable resources, but the level of their future use

will depend on the technological and economic performance of technologies

feeding on these flows as well as on possible constraints on their use. The

long-term availability of energy resources will likely become more an issue of

the degree to which future societies want to balance environmental and economic

tradeoffs, control greenhouse gas emissions, and internalise externalities, or

of the technological and economic performance of different clean energy

conversion technologies, than a question of resource existence.

This chapter examines long-term energy resource availability

primarily from the perspectives of theoretical maximums, or ultimately

recoverable resources. Admittedly, it can be argued that an analysis based on

ultimately recoverable resources is irrelevant - hydrocarbon occurrences or

natural flows become resources only if there is demand for them and appropriate

technology has been developed for their conversion and use. Indeed, energy

resources generally should not be scrutinised without reference to the chain

extending from the extraction of resources to the supply of energy services -

that is, along all the conversion steps to the point of what consumers really

want: transportation, communication, air conditioning, and so on. But the

assessment in this volume has been structured so that each link of the chain is

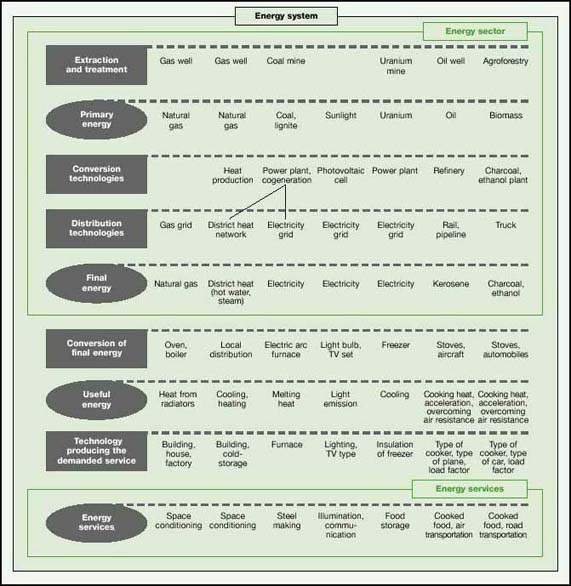

explored separately. Energy conversion technologies are discussed in chapters 7

(renewable energy technologies) and 8 (advanced fossil and nuclear energy

technologies), as well as in chapter 6 (energy efficiency).

Hydrocarbon occurrences become resources only if there

is demand for them and appropriate technology has been developed for

their conversion and use.

Definitions and units

A variety of terms are used to describe energy reserves, and

different authors and institutions have different meanings for the same terms.

Meanings also vary for different energy sources. The World Energy Council

defines resources as "the occurrences of material in recognisable form" (WEC,

1998). For oil, it is essentially the amount of oil in the ground. Reserves

represent a portion of resources and is the term used by the extraction

industry. British Petroleum notes that proven reserves of oil are "generally

taken to be those quantities that geological and engineering information

indicates with reasonable certainty can be recovered in the future from known

reservoirs under existing economic and operating conditions" (BP, 1999). Other

common terms include probable reserves, indicated reserves, and inferred

reserves - that is, hydrocarbon occurrences that do not meet the criteria of

proven reserves. Undiscovered resources are what remains and, by definition, one

can only speculate on their existence. Ultimately recoverable resources are the

sum of identified reserves and the possibly recoverable fraction of undiscovered

resources and generally also include production to date. Then there is the

difference between conventional and unconventional occurrences (oil shale, tar

sands, coalbed methane, clathrates, uranium in black shale or dissolved in sea

water), especially the rate at which unconventional resources can be converted

into conventional reserves.

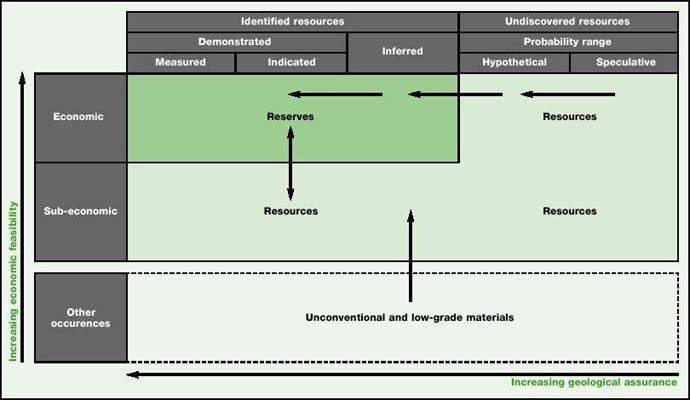

FIGURE 5.1. PRINCIPLES OF RESOURCE

CLASSIFICATION

Source: Based on McKelvey, 1967.

To the extent possible, this chapter uses the McKelvey box,

which presents resource categories in a matrix with increasing degrees of

geological assurance and economic feasibility (figure 5.1). This scheme,

developed by the U.S. Bureau of Mines and the U.S. Geological Survey (USGS,

1980), is to some extent also reflected in the international classification

system recently proposed by the United Nations.

In this classification system, resources are defined as

concentrations of naturally occurring solid, liquid, or gaseous material in or

on the Earth’s crust in such form that economic extraction is potentially

feasible. The geologic dimension is divided into identified and undiscovered

resources. Identified resources are deposits that have known location, grade,

quality, and quantity or that can be estimated from geologic evidence.

Identified resources are further subdivided into demonstrated (measured plus

indicated) and inferred resources, to reflect varying degrees of geological

assurance. Reserves are identified resources that are economically recoverable

at the time of assessment (see the British Petroleum definition, above).

Undiscovered resources are quantities expected or postulated to

exist under analogous geologic conditions. Other occurrences are materials that

are too low-grade or for other reasons not considered technically or

economically extractable. For the most part, unconventional resources are

included in ‘other occurrences’.

The boundary between reserves, resources, and occurrences is

current or expected profitability of exploitation, governed by the ratio of

market price to cost of production. Production costs of reserves are usually

supported by actual production experience and feasibility analyses, while cost

estimates for resources are often inferred from current production experience

adjusted for specific geological and geographic conditions.

Technological improvements are continuously pushing

resources into the reserve category by advancing knowledge and lowering

extraction costs.

For several reasons, reserve and resource quantities and related

supply-cost curves are subject to continuous revision. Production inevitably

depletes reserves and eventually exhausts deposits, while successful exploration

and prospecting add new reserves and resources. Price increases and cost

reductions expand reserves by moving resources into the reserve category and

vice versa. The dynamic nature of the reserve-resource relationship is

illustrated by the arrows in figure 5.1. Technology is the most important force

in this process. Technological improvements are continuously pushing resources

into the reserve category by advancing knowledge and lowering extraction costs.

The outer boundary of resources and the interface to other

occurrences is less clearly defined and often subject to a much wider margin of

interpretation and judgement. Other occurrences are not considered to have

economic potential at the time of classification. But over the very long term,

technological progress may upgrade significant portions to resources.

In 1992 the United Nations Economic Commission on Europe (UNECE)

launched an effort to define a generally applicable resource classification

scheme with a higher resolution of technical and economic feasibility than the

McKelvey box. By adding a third dimension - the level of actual feasibility of

extraction based on geological engineering assessments - this new classification

provides a more accurate picture of the accessibility of resources. In 1997 the

United Nations International Framework Classification for Reserves/Resources -

Solid Fuels and Mineral Commodities (UNFC) was completed and recommended by the

Economic and Social Council (ECOSOC) for world-wide application. But it will

take time for the UNFC to be universally adopted by public and private

institutions and for fossil reserves and resources to be consistently reported

in compliance with the UNFC.

For renewable energy sources, the concepts of reserves,

resources, and occurrences need to be modified. Renewables represent annual

flows available, in principle, on an indefinite sustainable basis. Fossil energy

reserves and resources, although expanding over time, are fundamentally finite

quantities. In this context the annual natural flows of solar, wind, hydro, and

geothermal energy and quantities grown by nature in the form of biomass (often

referred to as theoretical potentials) would correspond to occurrences. The

concept of technical potentials can be used as a proxy for energy resources,

while economic potentials correspond to reserves. The distinction between

theoretical and technical potentials reflects the degree of use determined by

thermodynamic or technological limitations without consideration of practical

feasibility or costs. Thus the economic potential is the portion of the

technical potential that could be used cost-effectively. In terms of reserves,

resources, and occurrences of hydrocarbons, economic and technical potentials

are dynamically moving targets in response to market conditions and technology

availability and performance.

This chapter reports oil resources in gigatonnes (1 Gt =

109 tonnes) and exajoules (1 EJ = 1018 joules) using the

energy equivalent of 42 gigajoules per tonne of oil equivalent (GJ per toe). Gas

resources are reported in tera cubic metres (1 Tm3 = 1012

cubic metres) and converted to EJ using 37 gigajoules per 1,000 cubic

metres (GJ per 1,000 m3). Coal resources are usually reported in

natural units, although the energy content of coal may vary considerably within

and between different coal categories. The Bundesanstalt f�r Geowissenschaften

und Rohstoffe (Federal Institute for Geosciences and Natural Resources, referred

to here as the BGR) in Hannover (Germany) is the only institution that converts

regional coal occurrences into tonnes of coal equivalent (1 tce = 29

gigajoules). Thus coal resource data come from the BGR. Uranium and other

nuclear materials are usually reported in tonnes of metal. The thermal energy

equivalent of 1 tonne of uranium in average once-through fuel cycles is about

589 terajoules (IPCC,

1996a).

Oil reserves and resources

Views on the long-term availability of oil and natural gas

continue to spark controversy and debate. One school of thought believes that

the best oil fields have already been discovered and that the amount of oil

still to be discovered is somewhat limited. The other school regards oil

reserves as a dynamic quantity, driven by demand and technological advances. The

second school is more optimistic about future hydrocarbon

availability.

Ultimately recoverable resources - the static or geologists’ view

For many years, world oil reserves have experienced small but

steady increases, which implies that the discovery or delineation of new

reserves has at least kept pace with production. But many geologists focus on

the concept of a quasi-fixed stock of hydrocarbon occurrences that, once

production commences, can only decrease. For oil, they argue that few new oil

fields have been discovered since the mid-1970s, and that most reserve increases

have come from revisions of previously underestimated existing reserves

(Hatfield, 1997; Campbell and Laherrere, 1998) and improved recovery techniques.

Peak production lags behind peak discovery (of the mid-1960s) by several

decades. Larger and more obvious fields are found first, leading to an early

peak in discovery and diminishing returns in exploration: the more that is

found, the less is left to find. Fields that are smaller and harder to find and

to exploit follow, but eventually the fixed stock will be exhausted. Some 90

percent of current global oil production comes from fields more than 20 years

old.

TABLE 5.1. ESTIMATED OIL RESERVES

Region

Identified reserves (Masters and others, 1994)

Identified reserves plus 95%a (Masters and

others, 1994)

Identified reserves plus modeb (Masters and

others, 1994)

Identified reserves plus 5%c (Masters and

others, 1994)

Proven recoverable reserves (WEC, 1998)

Proven reserves (BP, 1999)

Total resources from enhanced oil recoveryd

Gigatonnes

Exajoules

Gigatonnes

Exajoules

Gigatonnes

Exajoules

Gigatonnes

Exajoules

Gigatonnes

Exajoules

Gigatonnes

Exajoules

Gigatonnes

Exajoules

North America

8.5

356

14.3

599

17.0

712

23.7

992

4.6

193

4.6

193

13.6

569

Latin America and Caribbean

17.3

724

22.6

946

26.2

1,097

41.6

1,742

19.2

804

19.9

833

23.8

996

Western Europe

5.6

234

6.8

285

7.7

322

11.2

469

2.5

105

2.5

105

3.9

163

Central and Eastern Europe

0.3

13

0.4

17

0.5

21

1.1

46

0.3

13

0.2

8

0.5

21

Former Soviet Union

17.0

712

25.1

1,051

30.6

1,281

49.9

2,089

8.0

335

9.1

381

11.2

469

Middle East and North Africa

87.6

3,668

97.0

4,061

104.6

4,379

126.4

5,292

99.6

4,170

96.8

4,053

59.2

2,479

Sub-Saharan Africa

4.0

167

5.9

247

7.3

306

12.3

515

4.0

167

4.5

188

3.3

138

Pacific Asia

3.1

130

4.1

172

4.8

201

7.3

306

1.5

63

1.5

63

2.1

88

South Asia

1.0

42

1.1

46

1.3

54

1.8

75

0.8

33

0.5

21

0.6

25

Centrally planned Asia

5.1

214

7.8

327

9.8

410

17.9

749

5.4

226

3.4

142

3.7

155

Pacific OECD

0.4

17

0.6

25

0.7

29

1.3

54

0.4

17

0.4

17

0.5

21

Totale

150

6,277

186

7,776

210

8,812

295

12,329

146

6,126

143

6,004

123

5,124

Note: Excludes cumulative production to the date of

assessment. a. Identified reserves plus estimates of undiscovered resources with

a 95 percent probability of discovery. b. Identified reserves plus estimates of

undiscovered resources with a 50 percent probability of discovery. c. Identified

reserves plus estimates of undiscovered resources with a 5 percent probability

of discovery. d. Includes enhanced recovery of past and future oil production.

e. Totals rounded.

Cumulative production is a good proxy for geological knowledge

gained through exploration experience. All these facts leave no room for any

conclusion other than that peak production is being approached rapidly. In the

1960s ultimately recoverable resources became a popular concept for quantifying

the fixed stock of hydrocarbon occurrences. Ultimately recoverable resources

include cumulative production, proven reserves at the time of estimation, and

oil remaining to be discovered - in other words, the ultimate oil wealth

available to humans. For the past 40 years most estimates of ultimately

recoverable resources for conventional oil have ranged from 200 - 400

gigatonnes. More recently, Campbell and Laherrere (1998) put ultimately

recoverable reserves at about 250 gigatonnes, Hiller (1999) at 350 gigatonnes,

Edwards (1997) at 385 gigatonnes, Masters and others (1994) at 281 - 390

gigatonnes, and Odell (1997) at 410 gigatonnes. All these estimates include

production to the date of estimation (96 - 110 gigatonnes).

The debate on the size of ultimately recoverable resources and

the time horizon when the depletion midpoint will be reached includes only

conventional oil occurrences. Shale oil, tar sands (natural bitumen), and heavy

crude oil are considered unconventional oil resources, defined as occurrences

that cannot be tapped with conventional production methods for technical or

economic reasons or both (Rogner, 1997; Gregory and Rogner, 1998). These

resources form a large part of the vast store of hydrocarbons in the

Earth’s crust and, in the case of oil, have been assessed to be at least as

large as conventional oil resources (see below). The existence of unconventional

oil and gas is acknowledged by ‘fixed stock’ analysts, but they are

less sanguine about the future technological potential for bringing these

resources to market. Technological pessimism and an exclusive focus on

conventional oil largely explain the geologists’ view that global oil

production will reach its peak and mid-depletion point in the near future.

Conventional oil. Table 5.1 reports recent estimates,

excluding cumulative production to date, of identified or proven oil reserves

and natural gas liquids. All these estimates report reserves at around 1,000

billion barrels of oil (143 - 150 gigatonnes).

Masters and others (1994) estimate identified reserves on 1

January 1993 to be 150 gigatonnes (6,277 exajoules), only slightly higher than

British Petroleum and World Energy Council estimates of proven reserves at the

end of 1997.1 Masters and others also estimate undiscovered oil

resources based on a modified Delphi technique and geological analogies. Their

low estimate (95 percent probability of discovery) brings their total for

recoverable conventional oil reserves to 186 gigatonnes (7,771 exajoules). If

cumulative production until 1994 of 95 gigatonnes (3,990 exajoules) is added,

the total for ultimately recoverable resources is 281 gigatonnes (11,800

exajoules). The medium (mode) estimate of undiscovered resources brings total

recoverable oil reserves to 210 gigatonnes (8,812 exajoules) and ultimately

recoverable resources to 305 gigatonnes (12,810 exajoules). The high (5 percent

probability) estimate of undiscovered resources brings total recoverable oil

reserves to 295 gigatonnes (12,329 exajoules) and ultimately recoverable

resources to 390 gigatonnes (16,380 exajoules).

TABLE 5.2. ESTIMATED UNCONVENTIONAL OIL RESERVES AND

RESOURCES

Region

Oil shale

Heavy crude oil

Tar sands (natural bitumen)

Identified resources(BGR, 1998)

Total resources(BGR, 1998)

Proven recoverable and estimated additional reserves(WEC,

1998)

Oil in place(BGR, 1998)

Reserves and resources(BGR, 1998)

Future potential recovery(Meyer, 1997)

Oil in place(BGR, 1998)

Reserves and resources(BGR, 1998)

Proven recoverable and estimated additional reserves(WEC,

1998)

Gigatonnes

Exajoules

Gigatonnes

Exajoules

Gigatonnes

Exajoules

Gigatonnes

Exajoules

Gigatonnes

Exajoules

Gigatonnes

Exajoules

Gigatonnes

Exajoules

Gigatonnes

Exajoules

Gigatonnes

Exajoules

North America

1.1

48

351.6

14,767

217.0

9,114

15.7

659

2.3

96

2.0

82

233

9,786

40.7

1,710

51.7

2,173

Latin America and Caribbean

0.3

14

19.4

814

9.6

405

229.3

9,631

59.7

2,509

51.2

2,152

190

7,980

33.2

1,395

1.2

49

Western Europe

0.5

22

8.9

374

0.0

1

9.8

412

3.7

155

3.2

133

0

0

0.0

0

0.0

0

Central and Eastern Europe

1.1

45

2.8

116

0.0

0

0.1

4

0.1

5

0.1

5

0

0

0.0

0

0.0

0

Former Soviet Union

4.2

178

9.6

405

6.5

273

0.1

4

19.2

805

16.4

690

232

9,744

40.5

1,703

0.0

0

Middle East and North Africa

7.6

319

8.1

340

28.0

1,175

45.2

1,898

20.2

847

17.3

726

0

0

0.0

0

0.0

0

Sub-Saharan Africa

0.0

0

16.4

690

0.0

0

1.4

59

0.9

39

0.6

27

3

126

0.5

22

0.0

0

Pacific Asia

1.0

40

1.0

40

1.7

71

1.1

46

1.5

62

1.4

59

0

0

0.0

0

0.0

0

South Asia

0.0

0

0.0

0

0.0

0

1.0

42

0.0

2

0.0

1

0

0

0.0

0

0.0

0

Centrally planned Asia

0.6

25

20.0

840

0.0

0

10.8

454

2.6

111

2.3

95

0

0

0.0

0

0.0

0

Pacific OECD

3.8

160

44.5

1,870

36.0

1,513

0.0

0

0.0

1

0.0

1

0

0

0.0

0

0.0

0

Total

20.3

851

482.3

20,256

298.9

12,552

314.5

13,209

110.3

4,632

94.5

3,971

658

27,636

115.0

4,830

52.9

2,222

In its 1998 survey the World Energy Council reported proven

recoverable oil reserves of 146 gigatonnes (6,126 exajoules) and estimates

additional recoverable reserves (excluding speculative occurrences) of 28

gigatonnes (1,192 exajoules), for a total of 174 gigatonnes (7,318 exajoules).

This compares well with the Masters and others estimate of identified reserves

plus 95 percent probability of undiscovered resources of 186 gigatonnes. The oil

reserve estimates in table 5.1 reflect the views of geologists on the

availability of conventional oil and are consistent with the ultimately

recoverable resource estimates presented earlier.

Today only about 35 percent of the oil in place is recovered by

primary and secondary production methods. With enhanced oil recovery methods,

this rate can be increased to as much as 65 percent of the original oil in place

in a reservoir, though at higher extraction costs (BGR, 1995). Thus the

application of enhanced oil recovery methods in abandoned fields and new

developments increases conventional oil resources.

Table 5.1 shows the potential resources resulting from the use

of enhanced oil recovery techniques. Resources are calculated based on an

average recovery rate of 35 percent achieved in historical production and used

in the delineation of proven recoverable reserves, and an enhanced oil recovery

rate of 15 percent, for an overall recovery rate of 50 percent.

Unconventional oil. The vast amounts of unconventional

oil occurrences include oil shale, heavy crude oil, and tar sands.

Unconventional oil is already economic to exploit in some places, so some is

defined as reserves. Further development may depend on higher oil prices,

technological developments, and long-term demand for liquid fuels. According to

BGR (1998), reserves of unconventional oil could be as high as 245 gigatonnes,

substantially exceeding proven reserves of conventional oil (table 5.2).

Oil shale is a sedimentary rock rich in organic matter

containing more than 10 percent kerogen. It can be used directly as a fuel in

power plants or processed to produce synthetic petroleum products. The kerogen

content of oil shale varies widely. According to BGR (1995), only about 1

percent of world resources contains more than 100 litres of oil per cubic metre

rock, while 85 percent have less than 40 litres per cubic metre.

Data on oil shale resources are presented in table 5.2. The most

recent BGR (1998) estimate of oil shale resources is 482 gigatonnes, down from

920 gigatonnes in the 1995 estimate. WEC (1998) estimates recoverable and

estimated additional reserves at 299 gigatonnes. Major oil shale resources are

in China, Estonia, the United States, Australia, and Jordan. The large regional

differences between the BGR and WEC estimates are likely the result of different

definitions.

Because of the high costs of mining and processing, oil shale is

produced only in small quantities in China and Estonia. Estonia is the only

country with an economy dominated by oil shale as a source of energy and for

more than 70 years has been the largest user of oil shale in power generation.

Recent production totalled 20 million tonnes of oil shale a year (Hobbs, 1995).

Heavy crude oil is defined as high-viscosity crude oil

with a density equal to or less than 20° API (934 kilograms per cubic

metre). Extra heavy oil is crude oil with a density equal to or less than

10° API (1,000 kilograms per cubic metre). Unlike tar sands, the viscosity

of these hydrocarbons is below 10,000 millipoise (see below). Heavy oil is

formed by the degradation of conventional oil in shallow reservoirs.

Recent estimates of heavy oil resources are summarised in table

5.2. BGR (1995) estimates oil in place to be 315 gigatonnes. In BGR (1998), 33

of these are considered reserves and 77 are considered resources, for a total of

110 gigatonnes - well within the range of future potential recovery given by

Meyer (1997). About half of heavy oil resources are in Venezuela; the former

Soviet Union, Kuwait, Iraq, Mexico, and China account for most of the rest.

Meyer (1997) uses the term unproved reserves because his

estimates include some probable and possible reserves. Quantities stated under

undiscovered potential recovery include all resources based on geological and

engineering judgement, using a recovery factor of 10 percent.

Some 8 percent of world oil production come from heavy oil

reservoirs, with Venezuela, the United States, Canada, Iraq, Mexico, and the

former Soviet Union being major producers (BGR, 1998). Due to the nature of

heavy oil, enhanced oil recovery methods such as steam flooding and hot water,

polymer, and carbon dioxide injection are generally required for its extraction.

Tar sands (natural bitumen) and extra heavy oil

are sands or sandstones that contain a large portion of tarry hydrocarbons

with a viscosity exceeding 10,000 millipoise. They are formed by thermal

metamorphism and biodegradation of conventional oil deposits. The high viscosity

of these hydrocarbons requires unconventional extraction methods such as mining

with bucket-wheel excavators or in truck and shovel operations. Natural bitumen

typically contains large portions of sulphur and trace elements, including

vanadium and nickel.

BGR (1998) estimates that 115 of the 658 gigatonnes of tar sands

qualify as possible reserves (see table 5.2). Commercial production is limited

to the Athabasca tar sand deposits of Alberta (Canada), with a volume of 25

million tonnes in 1998 (WEC, 1998). To reduce the environmental disturbance

caused by surface mining, in situ techniques are increasingly used (box 5.1). In

addition, new extraction technologies, such as steam-assisted gravity drainage,

are being developed to reduce oil viscosity through steam injection (George,

1998). The use of extra heavy oil has commenced in the Orinoco oil belt of

Venezuela (BGR,

1998).

Available resources - the dynamic or economists’ view

Unlike geologists, who tend to treat resources as an innate

component of the physical world, economists view what exists in the Earth’s

crust as ‘neutral stuff’ (Odell, 1998) that becomes a resource only if

there is a market demand for it. Put differently, "there are huge amounts of

hydrocarbons in the earth’s crust� (Adelman and Lynch, 1997), and

"estimates of declining reserves and production are incurably wrong because they

treat as a quantity what is really a dynamic process driven by growing

knowledge" (Nehring, 1998). Improvements in technology - such as

three-dimensional seismic surveys and extended-reach drilling - have allowed

higher recovery rates from existing reservoirs and the profitable development of

fields once considered uneconomic or technically beyond reach, expanding the

boundary of reserves and shifting resources into the reserve category.

BOX 5.1. ENVIRONMENTAL OBSTACLES TO EXTRACTING

UNCONVENTIONAL OIL

The production of unconventional oil and the necessary upgrade

to marketable fuels can hurt local environments. Mining, conversion, and

upgrading to synthetic crude oil can produce toxic heavy metals and large

quantities of solid and acidic liquid and gaseous wastes that need to be

contained, cleaned, and disposed ofin an environmentally benign manner. This may

require stringent environmental controls and new policies for toxic waste

disposal. Extracting hydrocarbons from unconventional oils such as tar sands,

heavy oils, and oil shale involves very large surface (open-pit or strip) mining

and underground mining (room and pillar technique), steam soaking, steam

flooding, or in situ combustion. Here the production of tar sand and its

upgrading to synthetic crude oil are used to show the potential environmental

constraints of large-scale unconventional oil production.

The production of synthetic crude oil from Alberta,

Canada’s tar sand deposits involves open-pit mining and handling of 5

tonnes of tar sands and overburden per barrel of oil produced (Penner and

others, 1982), milling to separate the bitumen from the sand, and upgrading it

to commercial quality. Syncrude, a Canadian company, processes 510,000 tonnes of

tar sands a day and recovers about one barrel of heavy oil for every 2 tonnes of

tar sands processed (Stosur and others, 1998). A hot water process is the most

common for extracting oil from the sand. The process is energy-intensive and

requires large quantities of hot water. Syncrude operations require 1,400 tonnes

an hour of water heated to nearly 500 degrees Celsius. Water is recycled to the

maximum extent (90 percent). The remaining materials (tailings) after the

bitumen has been extracted (extraction rate some 90 percent)are liquids and

sand. Most of the tailings are the excavated overburden rock and rejected sand;

both can be stockpiled and used as backfill with little threat to the

environment (Stosur and others, 1998).

Things are different for the liquid tailings, which are

contaminated with organic and inorganic compounds (sulphur, porphyrins, salts of

organic acids) and can seriously damage nearby aquatic ecosystems. The liquid is

stored in settling ponds, allowing water to clarify before it is recycled. These

ponds are designed as ‘zero discharge’ basins, and no process-affected

water is discharged in running waters. But while tailings sand settles out

quickly, the fine-grained materials (silts and clays) and residual bitumen

consolidate slowly and can pose a long-term problem and liability. Tailings

ponds must be constructed to last several decades and must be guarded against

erosion, breaching, and foundation creep until better disposal practices become

available (Stosur and others, 1998). New processes such as dry retorting - which

generates dry tailings - are expected to minimise the risk of acid drainage from

tar sand tailings. Other methods include faster consolidation of fine tailings,

detoxification of tailing pond water, and reprocessing of fine tailings

(including co-production of minerals and metals).

Spent tar sand (mainly sand, silt, and clay contaminated with

the remaining bitumen and caustic compounds) is put in specially designed

storage areas to avoid acid drainage or used as fill material in mine

reclamation efforts. While the disrupted land area can be considerable, land

reclamation is usually imposed on mine operators to limit permanent

environmental damage and to return land to a stable, biologically

self-sustaining state.

Upgrading operations are the primary source of airborne

emissions. Sulphur dioxide, particulates, hydrocarbons, vanadium, and nickel

were originally of major concern. In addition, bitumen contains several

carcinogenic polycyclic aromatic hydrocarbons (WHO, 1982). Hydrotreaters remove

sulphur and nitrogen and produce elemental sulphur as a by-product. Nitrogen is

removed as ammonia and used as an under-boiler fuel or for chemical feedstock.

Hydrogen sulphide is removed from the by-product fuel gas that fuels parts of

the upgrading operations. The synthetic crude oil produced from Alberta’s

tar sand deposits is 32 - 33o API with 0.1 - 0.2 percent sulphur. It

contains no residue, while typical conventional crudes have about 8 percent

residue.

Stosur and others (1998) estimate that only 15 percent of tar

sand resources are suitable for surface mining. The rest would have to be

extracted by in situ methods, which minimise land disturbance through multiwell

pads and horizontal drilling (Sadler and Houlihan, 1998). To reduce odour and

greenhouse gas emissions, care must be taken to collect and reuse or flare the

gases generated by the process.

Alberta’s tar sand operations indicate that environmental

protection is the result of effective environmental regulation and controls,

including a balance of resource development and resource conservation and of

environmental and socioeconomic policies.

In addition, economists argue, a distinction between

conventional and unconventional occurrences is irrelevant. Today most

unconventional occurrences are neutral stuff and will become resources and

reserves if there is sufficient demand. In fact, certain unconventional

occurrences - heavy oil, tar sands, coalbed methane and gas from aquifers - have

already started to ‘come in from the margin’. Conventional discoveries

previously regarded as uneconomic can now be developed profitably, and

recoverable reserves can be increased in fields being developed or under

production. In short, economists view oil and gas reserves as a portion of the

total hydrocarbon occurrences contained in the Earth’s crust, where volumes

depend on exploration know-how to locate and evaluate a play (delineated

deposit) and on the capability of technology to extract it at an acceptable cost

given sufficient demand.

The question of long-term hydrocarbon resource availability,

then, is viewed from the perspective of anticipated demand in competitive

markets - taking into account technological change and growing knowledge. In the

presence of sufficiently large conventional oil reserves there is, at present,

no demand for the large-scale use of abundant unconventional oil occurrences

(see above). This explains the absence of any significant motivation for a

comprehensive and systematic evaluation of these resources or for the

development of technology for their economic and environmentally acceptable

recovery.

Economists take proven conventional oil reserves of 150

gigatonnes as a point of departure that, based on their definition, can be

brought to the market at post-1986 price levels. In addition, economists point

to industry expectations that proven reserves will grow 50-70 gigatonnes by 2020

(Shell, 1996). They point out that the oil industry has historically responded

to demand by finding and developing reserves, even given the long lead time for

this process: since World War II it has taken more than 40 years to move from

identifying reserves to producing resources. This is seen as a clear indication

that the process of stock replenishment is working effectively.

A bigger role for unconventional oil. Economists also

argue that unconventional oil should be viewed as an important element of the

oil resource base - and after 2030 it will be a critical complement to

conventional oil production in keeping the oil supply curve moving upwards. This

long process of the changing supply pattern will be seamless from the viewpoint

of oil producers. From the point of view of users the process will be

unimportant, because no essential difference will arise for them merely because

of the changing nature of exploitation of oil habitats in the Earth’s

surface. In precisely the same way, today’s oil consumers do not need to

consider whether their supply is from shallow or deep horizons, or from onshore

or offshore locations.

The oil industry has historically responded to demand by

finding and developing reserves, even given the long lead time for this

process.

The ultimate resource base of unconventional oil is irrelevant

to the 21st century’s energy supply. Occurrences of such oil that are

already known and under exploitation can provide the global supply likely to be

required in the 21st century. On the other hand, economic or environmental

considerations - or both - could convert unconventional resources back to

neutral stuff, as has occurred in recent decades with previously designated coal

resources.

Costs and technological developments. New technologies

for exploring and extracting oil have lowered exploration, development, and

production costs while expanding the oil resource base. Further advances in

technology must also be expected, resulting in additional reductions in cost.

Part of these productivity gains will be offset by the use of more remote,

harder-to-access, and smaller deposits. Still, it appears plausible that

technological progress will continue to keep production costs in check.2

The technology learning curve for synthetic crude oil production from tar

sands in Alberta is a good example of the impact of technology on production

costs. In 1978 a barrel of synthetic crude oil cost about $26 a barrel. By 1996

breakthroughs in the technology for producing and refining bitumen as well as

better operating procedures had lowered these costs to $9.60 a barrel (Polikar

and Cyr, 1998).

Two developments will likely put upward pressure on prices. The

first is the increasing volume of energy that will be demanded in the first half

of the 21st century. The second is the significantly increased cash flows

required by the international oil industry to sustain enhanced investment in the

initial large-scale exploitation of rapidly increasing volumes of unconventional

oil and gas. In the 1950s the ability of consumers to secure large volumes of

international oil depended on the super-normal profits that the industry was

able to generate. More recent breakthroughs for gas in Europe and elsewhere were

likewise achieved because of super-normal profitability in the industry. After

2030, following the introduction to global markets of large-scale unconventional

hydrocarbons, prices should fall back as the long-run supply prices of the two

commodities once again start to decline under conditions of advancing technology

and increasing economies of scale (Odell,

1998).

Reconciling the two views

The differences between geologists’ (static) and

economists’ (dynamic) views of oil resources can be partly explained by the

way the different schools view unconventional oil. Geologists draw a strict line

between conventional oil (the oil they look for) and unconventional oil (the oil

that does not fit their template). Although some unconventional oil is being

exploited economically, geologists take a conservative view of its long-term

commercial viability. In contrast, economists consider irrelevant the dividing

line between conventional and unconventional oil. They anticipate a seamless

transition from one to the other as long as demand and market prices allow for a

profitable return on investment. In that case, unconventional occurrences

estimated to exist in the Earth’s crust (see table 5.2) would extend the

oil age well beyond the mid-21st century. Without demand, the issue of resource

availability becomes meaningless and unconventional oil occurrences remain

neutral stuff.

A historical review of the most popular guideline for the

industry, the ratio of reserves to production, puts into perspective the two

schools of thought. This ratio compares known reserves and current production

and so measures the temporal reach of exhaustible energy reserves. These ratios

typically fluctuate between 20 and 40 years.

But the notion of a reserve-to-production ratio is seriously

flawed and, in the past, has led to aberrant conclusions (MacKenzie, 1996). The

most erroneous conclusion is that the world will be running out of reserves by

the time suggested by the ratio.3 For oil, ratios of 20 - 40 years

have existed since the early 20th century (figure 5.2). According to this ratio,

the world should have run out of oil a long time ago. Instead, driven by

economics (in essence, demand for oil), advances in geoscience, and

technological progress in upstream production, reserves have been continuously

replenished from previously unknown sources (new discoveries) or technologically

or economically inaccessible occurrences. Although reserve additions have

shifted to more difficult and potentially more costly locations, technological

progress has outbalanced potentially diminishing returns.

FIGURE 5.2. RATIO OF RESERVES TO

PRODUCTION FOR CONVENTIONAL CRUDE OIL, 1900 - 98

Source: Adapted from BP, 1998.

New technologies for exploring and extracting oil have

lowered exploration, development, and production costs while expanding

the oil resource base.

Gas reserves and resources

Unlike oil, gas is not subject to controversy on estimates of

ultimately recoverable reserves. Proven reserves are comparable to those of oil

but high relative to current and cumulative production. Still, natural gas is

often viewed as the poor stepsister of oil. The development of natural gas

fields requires large investments in transmission and distribution

infrastructure.4 As a result gas discoveries, especially in

developing countries, are often not reported. But this does not imply a lack of

gas occurrence - in fact, over the 21st century there is enormous potential for

major gas

discoveries.

Conventional gas

The most recent estimates of conventional gas reserves come from

WEC (1998) for the end of 1996 and BP (1998) for the end of 1998. WEC gives

total reserves as 177 Tm3 (6,534 exajoules) at the end of 1996, 147

Tm3 (5,450 exajoules) of which were proven recoverable reserves

(table 5.3). The rest were additional recoverable reserves. The International

Gas Union (IGU, 2000) reports total potentially recoverable reserves as high as

502 Tm3 (18,390 exajoules).

Reserves have generally increased from survey to survey,

reflecting dramatic changes in the economics of gas exploration and recovery.

Reservoirs are being added in areas previously thought to have been exhausted,

and new reservoirs that were previously overlooked or ignored are now being

developed. Over the past 10 years reserve additions averaged 3.7 Tm3

(134 exajoules) a year, much higher than the 1997 production of 2.2

Tm3. Ivanhoe and Leckie (1993) note that fewer gas than oil fields

are reported in developing regions, probably because gas has a lower economic

and utility value, not because there are fewer gas fields.

Enhanced gas recovery using advanced recovery methods - notably

hydraulic fracturing aimed at improving the permeability of reservoir rock - can

substantially increase natural gas recovery in abandoned fields and newly

developed reservoirs. Another, more innovative technique, horizontal air

drilling, can also increase gas recovery in depleted gas zones (Elrod, 1997).

Estimates of potential reserves of natural gas resulting from

enhanced gas recovery are based on a historical average gas recovery rate of 50

percent and an enhanced recovery rate of 30 percent, for a total recovery factor

of 80 percent. Schollnberger (1998) uses similar assumptions in an assessment of

possible reserve development through 2100. Global cumulative natural gas

production through 1998 totalled 62 Tm3 (2,276 exajoules). Applying

an average recovery factor of 50 percent leads to an original amount of 124

Tm3. Enhanced gas recovery of 30 percent then enlarges reserves by 37

Tm3. Likewise, enhanced gas recovery reserves from future production

are estimated at 106 Tm3 using WEC (1998) total recoverable reserves

of 177 Tm3 (see table 5.3). Thus total potential natural gas reserves

available from enhanced oil recovery methods are estimated at 143 Tm3

(5,290 exajoules), an amount only slightly lower than proven natural gas

reserves and almost identical to the potential crude oil reserves expected from

enhanced recovery

methods.

Unconventional gas

BGR (1995) defines unconventional gas as natural gas derived

from reservoirs not exploitable by conventional recovery techniques.

Unconventional gas types include coalbed methane, tight formation gas, gas

hydrates (clathrates), and aquifer (geopressured) gas. Regional estimates of

unconventional gas occurrences in place are provided in table 5.4. The total

resource potential exceeds 25,000 Tm3 (960,000 exajoules).

Coalbed methane. Coalbed methane is a natural gas mixture

containing more than 90 percent methane. It occurs primarily in high-rank coal

seams from where it can migrate into the surrounding rock strata. Methane

contents in coal seams can range from traces to 25 cubic metres per tonne of

coal (Davidson, 1995). Regional resources of coalbed methane are genetically

associated with the geographic distribution of bituminous coal and anthracite

deposits. The former Soviet Union accounts for nearly 50 percent of recoverable

resources, centrally planned Asia (including China) has about 20 percent, and

North America has 15 percent.

Coalbed methane can be a by-product of underground coal mining

or be produced for the methane exclusively. In fact, coalbed methane is an

explosive hazard in underground mining operations and for safety reasons has

traditionally been vented with mines’ fresh air circulation. Since the

1970s methane captured from underground mining has increasingly been used to

supplement local gas supplies. Thus methane capture and use can significantly

mitigate greenhouse gas emissions because it avoids the release of methane - a

potent greenhouse gas - and may replace fossil fuels with a higher carbon

content. For long-term and stable methane supplies from coalbeds, however,

dedicated drilling in coalbeds is more important than the methane from active

underground coal mines.

Commercial coalbed methane production occurs only in the United

States, contributing about 5 percent to natural gas production (BGR, 1998). But

pilot projects are under way in a number of other countries, including

Australia, China, India, Poland, Russia, Ukraine, and the United Kingdom.

Estimates of methane resources range from 85 - 262 Tm3 (BGR, 1995,

1998; Rice, Law, and Clayton, 1993). This assessment uses the BGR (1995)

estimate of 233 Tm3 (see table 5.4).

Tight formation gas. Tight formation gas is natural gas

trapped in low-permeability reservoirs with in situ permeability of less than

0.1 millidarcy (mD), regardless of the type of the reservoir rock (Law and

Spencer, 1993). Production of tight gas requires artificial stimulation

techniques - such as massive hydraulic fracturing - to improve reservoir

permeability. An advanced technique is horizontal drilling to develop tight gas

formations, often in combination with massive hydraulic fracturing. These

stimulation methods can achieve gas flow rates two to three times those of

conventional vertical wells. In recent years about 3 percent of natural gas

production has come from tight gas reservoirs.

TABLE 5.3. ESTIMATED NATURAL GAS RESERVES

Region

Proven recoverable reserves(WEC, 1998)

Total recoverable reserves(WEC, 1998)

Proven and additional reserves(IGU, 2000)

Proven reserves(BP, 1999)

Enhanced gas recovery

Exajoules

Tm3

Exajoules

Tm3

Exajoules

Tm3

Exajoules

Tm3

Exajoules

Tm3

North America

252

6.8

389

10.5

2,307

63.0

244

6.6

884

23.9

Latin America and Caribbean

303

8.2

426

11.5

1,556

42.5

298

8.0

306

8.3

Western Europe

181

4.9

300

8.1

436

11.9

177

4.8

306

8.3

Central and Eastern Europe

26

0.7

26

0.7

77

2.1

17

0.5

45

1.2

Former Soviet Union

2,087

56.4

2,583

69.8

5,767

157.5

2,112

56.7

1,923

52.0

Middle East and North Africa

2,076

56.1

2,250

60.8

5,343

149.5

2,065

55.4

1,421

38.4

Sub-Saharan Africa

155

4.2

155

4.2

238

6.5

161

4.3

93

2.5

Pacific Asia

207

5.6

207

5.6

798

21.8

196

5.3

158

4.3

South Asia

63

1.7

63

1.7

377

10.3

54

1.5

50

1.4

Centrally planned Asia

48

1.3

48

1.3

641

17.5

82

2.2

41

1.1

Pacific OECD

56

1.5

89

2.4

850

23.2

47

1.3

62

1.7

Total

5,450

147.3

6,534

176.6

18,390

502.2

5,454

146.4

5,290

143.0

TABLE 5.4. ESTIMATED UNCONVENTIONAL NATURAL GAS RESOURCE

POTENTIAL IN PLACE

Region

Coalbed methane

Tight formation gas

Gas hydrates

Geopressured gas

Total unconventional gas

Exajoules

Tm3

Exajoules

Tm3

Exajoules

Tm3

Exajoules

Tm3

Exajoules

Tm3

North America

2,898

78

518

14

80,575

2,178

109,964

2,972

193,955

5,242

Latin America and Caribbean

0

0

222

6

57,331

1,549

103,341

2,793

160,894

4,348

Western Europe

168

5

222

6

19,806

535

27,861

753

48,057

1,299

Central and Eastern Europe

126

3

37

1

0

0

6,623

179

6,786

183

Former Soviet Union

2,646

72

1,665

45

151,533

4,095

73,667

1,991

229,511

6,203

Middle East and North Africa

0

0

925

25

4,788

129

67,784

1,832

73,497

1,986

Sub-Saharan Africa

42

1

111

3

4,788

129

63,677

1,721

68,618

1,854

Pacific Asia

210

6

148

4

0

0

45,103

1,219

45,461

1,229

South Asia

42

1

37

1

4,788

129

17,427

471

22,294

602

Centrally planned Asia

2,058

56

333

9

0

0

27,824

752

30,215

817

Pacific OECD

420

11

37

1

23,857

645

56,166

1,518

80,480

2,175

Total

8,610

233

4,255

114

347,467

9,391

599,437

16,201

959,769

25,940

Source: BGR, 1995, 1998; Rogner,

1997.

Although tight gas reservoirs exist in many regions, only the

tight gas resources in the United States have been assessed. The U.S. potential

of tight gas resources from tight sandstone and Devonian shale reservoirs is

13.4 Tm3 (BGR, 1995). BGR (1998) applies these U.S. estimates to

extrapolate tight gas resource potential for other countries and regions,

arriving at a global potential of 114 Tm3 (see table 5.4).

Gas hydrates. IGU (1997) includes some unconventional gas

in its definition of additional recoverable reserves - those that are at least

of foreseeable economic interest and that may prove technically and economically

recoverable with a reasonable level of confidence. This definition appears to

exclude gas hydrates (clathrates). IGU (1997) notes that:

Current scientific inquiries around the world are

considering gas hydrates as a potential future supply of natural gas. The

hydrates are frozen ice-like deposits that probably cover a significant portion

of the ocean floor. The extent of their coverage and the high methane content of

gas hydrates motivate speculation about the gigantic quantities of methane that

could become available. At the present time there has been no attractive

proposal for a technique to allow this methane to be recovered. Nor has there

been any scientific confirmation of the quantities of methane that might be

involved. Nevertheless, such investigations might bear fruit at some stage and

radically alter current ideas regarding natural gas availability.

The existence of gas hydrates has been confirmed by direct

evidence through sampling and by indirect evidence through geochemical and

geophysical investigations. Samples have been recovered in 14 parts of the

world; indirect evidence has been found in 30 others. Many oceanic occurrences

have been inferred based on a special geophysical exploration technique -

bottom-stimulating reflection. Resource estimates for gas hydrates are highly

uncertain. BGR (1998) reports global clathrate occurrences of more than 9,000

Tm3 (see table 5.4). Other estimates report clathrates as high as

20,000 Tm3 (MacDonald, 1990a, b; Collet, 1993).

There are no economically attractive technological proposals for

recovering methane hydrates (box 5.2). But given their enormous resource

potential, it is plausible to expect that extraction methods will eventually be

developed if long-term global gas demand warrants clathrate recovery. Research

projects are under way in India, Japan, and the United States to examine the

viability of gas hydrate recovery (Collet and Kuuskraa, 1998; BGR, 1998).

Aquifer (geopressured) gas. In many parts of the world,

natural gas is found dissolved in aquifers under normal hydrostatic pressure,

primarily in the form of methane (Marsden, 1993). This unconventional gas is

also referred to as hydropressured gas or brine gas. The amount of gas dissolved

in underground liquids increases substantially with depth. At depths up to 4,000

metres, 0.5 - 1.5 cubic metre of gas is dissolved per metre of water in

aquifers. This gas factor jumps to 7 - 20 at depths of 7,000 - 8,000 metres

(BGR, 1995).

Aquifer gas is expected to occur in nearly all sedimentary

basins (Marsden, 1993). While no detailed assessment of aquifer gas resources is

available, BGR (1998) derives potential aquifer gas in place from the

groundwater volume contained in high-permeability sand stones in the

hydrosphere. This approach leads to an estimate of 2,400 - 30,000 Tm3

of geopressured gas in place, with a mean estimate of 16,200

Tm3. In the absence of a more detailed assessment, a practical

approach had to be taken in delineating regional resource quantities. The

regional breakdown in table 5.4 was obtained by weighting the global mean

estimate of gas occurrence in place with regional shares of total sedimentary

area.

While these estimates of aquifer gas occurrences are highly

speculative, the potential quantities are staggering. Even a future recovery

factor of 5 percent implies a resource volume five times the conventional

reserves estimates of BP. Aquifer gas is already produced in small quantities

from shallow reservoirs in Italy, Japan, and the United States. But in all cases

aquifer gas recovery has been motivated by the production of trace elements

(such as iodine) rather than by the gas

itself.

Coal reserves and resources

Coal deposits can be found in sedimentary basins of various

geological ages. Mineable coal deposits require a minimum seam thickness over a

sufficiently large area. Coal production occurs in open-pit extraction or

underground mining. Coal resource estimates are generally based on drill-hole

tests and geological observations. Coal is subdivided into several broadly

defined types according to their caloric values. Generally, the types are

bituminous coal (including anthracite), sub-bituminous coal, and lignite. For

practical purposes, the subdivision is based on energy content, with the value

of 16,500 kilojoules per kilogram as demarcation between hard coal (bituminous

and high-energy sub-bituminous coals) and soft brown coal (lignite and

low-energy sub-bituminous coals).

For almost 200 years coal has provided the basis for energy

production as well as iron and steel manufacturing. It also fuelled the

industrial revolution of the 19th century. In the 20th century - mainly after

World War II - coal lost its leading position to crude oil. But the welfare and

economic development of many countries continue to be based on coal. Coal

provides about 22 percent of the world energy supply and is the most important

fuel for electricity generation. About 40 percent of global electricity is

produced in coal-fuelled power stations.

The differences between static and dynamic views of oil

resources can be partly explained by the way the different schools

view unconventional oil.

Coal will likely contribute substantially to the future world

energy supply. Assuming no intervention policies targeted at preventing climate

change, projections by IEA (1998c) and Nakicenovic, Gr�bler, and McDonald (1998)

show global coal production increasing from 2.4 gigatonnes of oil equivalent

(Gtoe) in 1995 to 4.0 Gtoe by 2020. Given its enormous proven reserves, the

current rate of coal production could continue well into the future.

The size of coal resources is not a restraining factor to its

use throughout the 21st century. Rather, continued coal use will depend on the

timely development of production facilities and related infrastructure, given

lead times of up to five years for open-cast operations and drift mines.

Nevertheless, there is considerable potential for a significant increase in coal

production capacity in the short to medium term. Although environmental

considerations may limit coal use with current combustion technologies, advanced

conversion technology - with carbon abatement and disposal - may create new

market opportunities (see chapter

8).

Current resources and reserves

World coal resources in place are estimated at more than 7,400

billion tonnes of coal, or about 4,470 Gtoe (WEC 1998). The recoverable portion

is estimated at roughly 500 Gtoe, which corresponds to the amount generally

labelled reserves. About 85 percent of the resources in place are classified as

bituminous or sub-bituminous (hard) coal; the rest is lignite (soft brown) coal.

(Similar proportions apply to reserves.)

BOX 5.2. ARE GAS HYDRATES AN EXPLOITABLE ENERGY

RESOURCE?

A gas hydrate is a crystalline cage of water molecules that can

trap various gases. Hydrates can form under conditions of high pressure and low

temperatures. Methane hydrates exist in polar permafrost and in sediments below

the ocean floor where conditions are appropriate. Hydrates will not exist below

a depth where the reservoir temperature is too high for their stability. But

solid hydrate layers can provide top seals for reservoirs of free methane that

can accumulate beneath. Offshore methane hydrate deposits have been identified

near the coasts of many countries - including countries (such as Japan)

otherwise poor in fossil fuels.

The amount of methane associated with hydrates is highly

uncertain, but the quantities are probably far greater than conventional oil and

gas resources combined. Estimates of global methane hydrate resources range from

0.1 - 300 million exajoules (Collet and Kuuskraa, 1998; Max, Pellanbarg, and

Hurdle, 1997). How much can be practically and affordably recovered is also

highly uncertain (USDOE, 1998). An emerging view is that free gas trapped

beneath solid hydrate layers will be easier to recover than gas in hydrates

(Max, Pellanbarg, and Hurdle, 1997). Free gas recovery would depressurise the

reservoir, leading to hydrate melting at the hydrate - free gas interface and

thus to free gas replenishment. The process could continue as long as the

hydrate layer remains thick enough to cap the free gas below. Preliminary

(though dated) estimates for recovering methane at favourable sites suggest that

it might not be significantly more costly than recovering conventional natural

gas (Holder, Kamath, and Godbole, 1984). But even if this proves accurate,

getting the gas to major markets could often be quite costly because of high

transport costs, since hydrate deposits are often far from such markets.

Three-quarters of global coal reserves are in Australia, China,

India, South Africa, and the United States. Among regions, North America has the

largest coal reserves (table 5.5). Substantial reserves are also available in

the former Soviet Union and in South Asia. The European share has to be viewed

with caution because reserves may soon be declassified to resources (neutral

stuff) as production subsidies are eliminated and industry begins to close

unprofitable operations.

In 1997 global coal production totalled 2,310 Gtoe, 91 percent

of which was hard coal. China was the largest producer of hard coal (31 percent

of the world total), followed by the United States (26 percent), India (7

percent), Australia (6 percent), and South Africa (6 percent). All other

producers hold shares of less than 5 percent.

Almost 90 percent of world coal production is used domestically.

In 1997 the 10 largest coal exporters traded about 500 million tonnes of hard

coal. The largest exporter was Australia with a traded share of about 30

percent, followed by the United States with 15 percent.

TABLE 5.5. ESTIMATED COAL RESERVES (MILLIONS OF TONNES)

Region

Bituminous (incl. anthracite)

Sub-bituminous

Lignite

Total (exajoules)

North America

115,600

103,300

36,200

6,065

Latin America and Caribbean

8,700

13,900

200

533

Western Europe

26,300

600

47,700

1,178

Central and Eastern Europe

15,400

5,500

10,700

744

Former Soviet Union

97,500

113,500

36,700

4,981

Middle East and North Africa

200

20

0

6

Sub-Saharan Africa

61,000

200

< 100

1,465

Pacific Asia

900

1,600

5,100

10

South Asia

72,800

3,000

2,000

1,611

Centrally planned Asia

62,700

34,000

18,600

2,344

Pacific OECD

48,100

2,000

41,600

1,729

Total

509,200

277,600

198,900

20,666

Source: WEC, 1998.

Projections show global coal production increasing from

2.4 Gtoe in 1995 to 4.0 Gtoe by 2020.

Additional resources

WEC (1998) also provides information on coal resources by type.

But because of incomplete country coverage, no regional or global aggregates are

given. BGR (1995) estimated global coal resources at 5,000 Gtoe, of which 4,600

Gtoe are hard coal. In a 1998 update, BGR revised the estimate for additional

coal resources in place to 4,300 Gtoe billion, of which about 3,500 Gtoe are

additional hard coal resources. The Russian Federation has the largest share -

about 2,100 Gtoe of hard coal. About 80 percent of the additional resources in

the Russian Federation are in remote areas of Siberia. Large investments for

infrastructure and development limit the conversion of these resources into

reserves. Because of the large reserves, there is no immediate need for

additional investigation of the resource potential world-wide. Estimates of the

regional distribution of world total resources (including reserves) are shown in

table

5.6.

Summary of fossil resources

Fossil fuel reserves, resources, and additional occurrences are

shown relative to cumulative consumption and current (1998) use in table 5.7.

For an analysis that extends well into the 21st century and explores the

long-term availability of fossil resources, the fossil resource base is the

relevant yardstick. The resource base for conventional and unconventional oil

and gas is large enough to last comfortably for another 50 - 100 years - and

possibly much longer - essentially at prices not much different from today. This

projection assumes that past hydrocarbon productivity gains in the upstream

sector can be maintained and that these resources remain in demand.

Tapping into the vast fossil resource base may eventually become

a transportation challenge. For one thing, fossil resources are not evenly

distributed around the globe. For another, the location of many unconventional

oil and, more important, gas occurrences is far from the centres of energy

demand. In China and India coal delivery costs (for rail transport) already

approach production costs. Transportation logistics and costs may affect the

economic attractiveness of remote resource sites. Long-distance and

trans-boundary energy transport raises concerns about the security of energy

supply (see chapter 4).

The fossil resource data in table 5.7 are also shown in terms of

their carbon content. Since the onset of the industrial revolution, 296

gigatonnes of carbon contained in fossil fuels have been oxidised and released

to the atmosphere. The resource base represents a carbon volume of some 6,500

gigatonnes of carbon. The 296 gigatonnes of carbon emitted to the atmosphere